Automated data entry is all about using smart software to pull information from documents and pop it right into your systems, no hands required. When it comes to bank statements, the best approach uses tools with AI-powered Optical Character Recognition (OCR). This tech can literally read the PDF statements and dump all that data neatly into an Excel sheet for you.

Why Manual Data Entry Is Costing You More Than Time

Before we get into the "how-to," let's talk about the "why." If you're still relying on manual data entry for bank statements, you're not just moving slowly—you're dealing with a serious business liability that silently eats up resources and creates unnecessary risk. The cost goes way beyond an employee's hourly wage.

Think about the classic process: someone stares at a PDF, then types those numbers into a spreadsheet. It’s a minefield of potential errors. Every single keystroke is a chance for a mistake, and one misplaced decimal point can throw off everything. Suddenly, you’re looking at flawed financial reports, incorrect tax filings, or making business decisions based on bad numbers. These aren't just little oopsies; they require hours of forensic accounting to track down and fix, blowing up the initial time investment.

The Hidden Costs of Human Error

Let's be real: people make mistakes. It's unavoidable in any manual process, especially when you're dealing with dense financial documents. Fatigue and repetition are the perfect recipe for typos. A simple number flip—transposing a 9 for a 6—can completely distort a month's financial picture, making your cash flow look way better or worse than it really is.

This unreliability sends ripples across the organization. Accountants can't trust the data without double-checking everything, which delays crucial reports. As a business owner, you might end up investing in a project that the (faulty) spreadsheet says is profitable, when it's actually a dud.

The real cost of manual data entry isn't just the salary you pay for the task. It's the organizational drag created by data you can't trust. It locks your team in a reactive loop of checking and re-checking, instead of doing high-value work like analysis and strategy.

The Problem of Scale

Manual data entry just can't keep up as your business grows. More transactions mean more statements to process. The only solution is to throw more people at the problem, which sends your operational costs through the roof without actually making the process any more efficient. It’s a linear solution to an exponential problem.

This puts a hard ceiling on your growth. You can't pay suppliers faster, reconcile accounts any quicker, or close the books on time. A sluggish financial back-office puts you at a huge disadvantage compared to nimble competitors who figured out automation a long time ago.

Despite these obvious downsides, you'd be surprised how many companies are stuck in the past. A recent study found that a staggering 49% of finance teams still rely entirely on manual processes with zero automation. Another 38% use older, clunky OCR tools that still need a ton of human hand-holding. That leaves a tiny fraction actually using fully automated systems. You can explore more data on finance automation adoption to see just how wide the gap is.

This gap is a massive opportunity. By adopting modern, AI-powered tools, you can leapfrog the limitations holding back nearly half of all businesses. The difference between the old way and the new way is night and day.

Manual vs. Automated Data Entry: A Quick Comparison

To put it in perspective, here's a quick side-by-side look at how the two methods stack up. The differences in speed, accuracy, and overall impact are stark.

| Feature | Manual Data Entry | Automated Data Entry |

|---|---|---|

| Speed | Slow, limited by human typing speed and attention span | Extremely fast, processes hundreds of pages in minutes |

| Accuracy | Prone to human errors like typos and transpositions | High accuracy, often exceeding 99.5% with AI-driven OCR |

| Scalability | Poor; requires hiring more staff to handle more volume | Excellent; handles increasing data volumes with no extra labor |

| Cost | High long-term labor costs and error-correction expenses | Higher initial setup, but low ongoing operational costs |

| Employee Focus | Tedious, repetitive work leading to low morale | Staff can focus on analysis, strategy, and verification |

Seeing it laid out like this makes the choice pretty clear. Automation doesn't just do the same job faster; it fundamentally changes what your team is capable of achieving.

Choosing the Right Automation Tool for Bank Statements

Picking a tool to pull data from bank statements isn't like choosing just any old software. You're handing it sensitive financial information, so the stakes are a lot higher. The market is packed with options, and it’s easy to get bogged down in feature lists that don't solve the real problem: dealing with all the different, and sometimes messy, bank statement PDFs out there.

The trick is to look past generic "OCR" claims and zero in on software that’s actually built with artificial intelligence. I’ve seen people get burned by older, template-based tools. They’re too rigid—the moment a bank tweaks its statement layout, the whole automation process falls apart. Modern, AI-powered solutions are different because they understand context. They can identify fields like "Date" or "Amount" no matter where they are on the page.

Core Features That Actually Matter

When you start comparing tools, you need to cut through the marketing fluff and focus on the features that will genuinely make your life easier. Your end goal is to get clean, structured data without a headache.

Here's what I consider non-negotiable:

- AI-Powered OCR: The tool has to be smart enough to read and make sense of different statement formats without you having to build a new template for every single bank. It should know a column of dates when it sees one.

- Multi-Page PDF Processing: Let's be real, most statements are more than one page long. The software should treat these documents as a single file, not a bunch of separate pages you have to manually piece together later.

- Clean Data Export: The final output, whether it's an XLSX or CSV file, needs to be well-structured and ready to go. You shouldn't have to waste time fixing merged cells, deleting stray text, or re-arranging jumbled columns.

A great automation tool doesn't just extract data; it delivers it in a format that's ready for analysis. The less time you spend on post-export cleanup, the higher your return on investment.

Asking the Right Questions Before You Commit

Before you pull out your credit card, run a few real-world tests. Pretend you have to process a year's worth of statements from three different banks. This kind of practical scenario will quickly show you a tool's strengths and, more importantly, its weaknesses.

Be sure to ask these specific questions:

- How does it handle different bank layouts? Can you feed it a statement from Chase and then one from a local credit union without having to reconfigure everything?

- What's the process for correcting errors? No system is 100% perfect. A good tool will have a simple interface that lets you make quick corrections right inside the app, which in turn helps the AI learn and get better.

- What are the security protocols? If it’s a cloud-based service, is your data encrypted both in transit and at rest? For desktop software, does it keep all the processing local on your machine?

This automation trend is exploding well beyond finance. For context, the broader marketing automation market was projected to hit $5.65 billion in 2024, with over two-thirds of marketers automating at least part of their workload.

Matching the Tool to Your Business Needs

The best tool for you really comes down to your specific situation. A solo entrepreneur handling ten statements a month has very different needs than a large accounting firm processing hundreds for multiple clients.

Think about these factors:

- Transaction Volume: How many statements or pages are you dealing with each month? Many tools are priced based on volume, so you’ll want to find one that fits your usage without breaking the bank.

- Technical Comfort: Are you looking for a simple, plug-and-play desktop app, or are you comfortable with a more powerful cloud platform that you can connect via an API?

- Integration Needs: Does this data need to get into your accounting software, like QuickBooks? If so, finding a tool with a built-in integration is a massive time-saver. For a wider view on how these systems can integrate, you might look into comprehensive ERP software solutions that tie together different parts of a business.

Choosing wisely from the start helps you avoid the common trap of picking a tool that’s either too basic for your needs or way too complicated to actually use. For more specific recommendations, our in-depth guide to https://bankstatementconvertpdf.com/bank-statement-software/ can help. By focusing on these practical points, you can find a solution that genuinely automates your financial data entry.

Building Your Automated Data Entry Workflow

Alright, let's get from theory to practice. This is where the magic really happens—where you actually build the system that turns a messy pile of bank statement PDFs into a clean, usable Excel spreadsheet. It’s less about complicated coding and more about connecting the dots in a logical way.

Think of it like this: you're a small business owner, and every month, PDF bank statements land in a specific Google Drive folder. The goal is to get all the transaction details—dates, descriptions, debits, and credits—into an Excel file for your accountant. And you want to do it without anyone touching a keyboard.

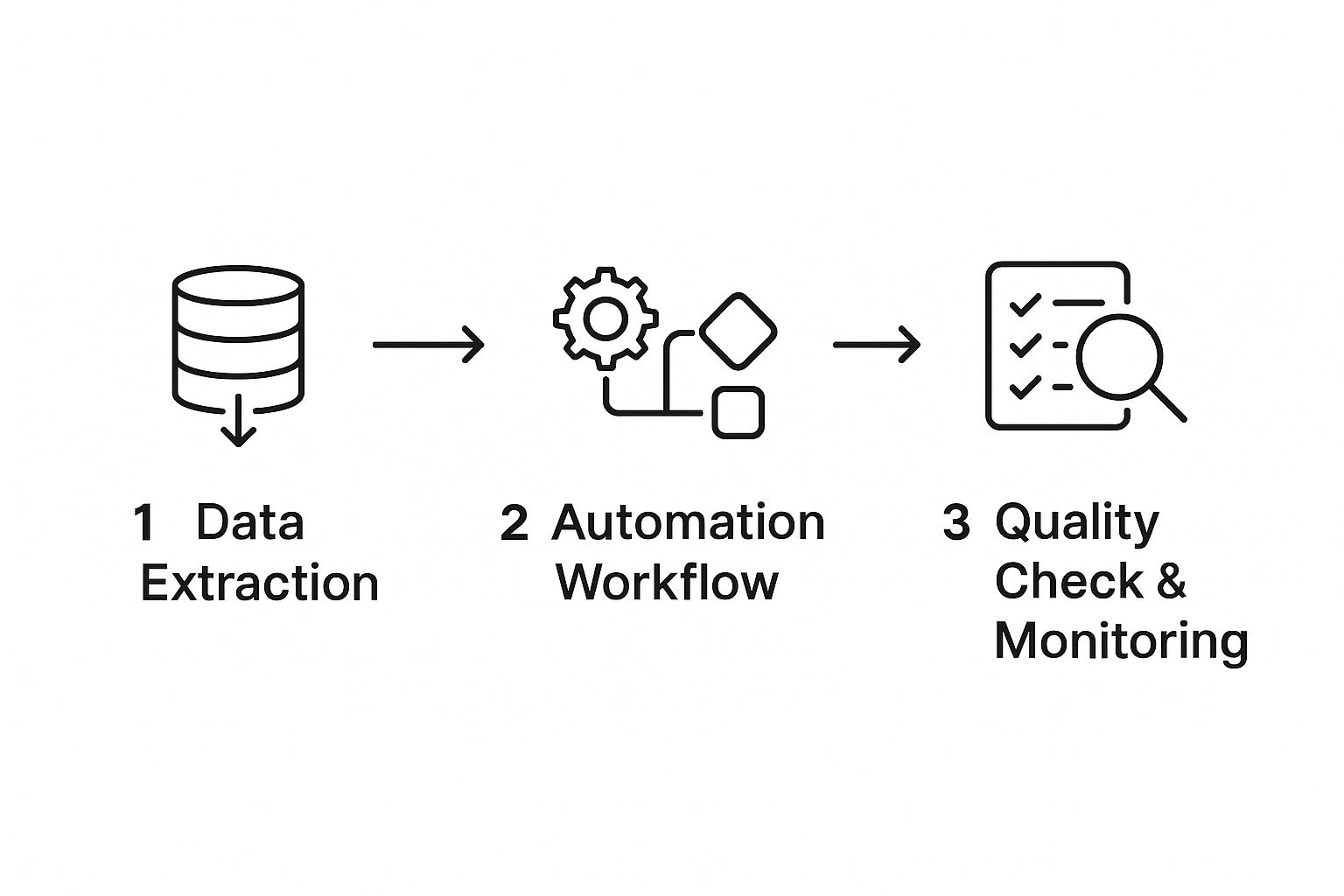

This is the kind of back-office efficiency that gives you back your time. The entire process really boils down to three main phases you'll set up.

As you can see, it's a straightforward journey from a raw document to clean data, driven by extraction, processing, and a quick final check.

First, Connect Your Document Source

The first practical step is simply telling the software where to find your bank statements. Think of it as creating a digital pipeline for your documents. Most modern tools are built to connect to the places you already keep your files, so this part is usually pretty painless.

You have a few common options for your source:

- A local folder: This could be a specific folder on your computer or a shared network drive where you dump all incoming statement PDFs.

- Cloud storage: This is often the most hands-off approach. You can link directly to services like Google Drive, Dropbox, or OneDrive. Once it’s set, you’re good to go.

- An email inbox: Some of the more advanced tools can even watch an email address for you. They’ll automatically grab any PDF attachments from emails with a specific subject line, like "Your Monthly Bank Statement."

For our business owner example, you’d connect the software to that "Monthly Statements" folder in Google Drive. It’s usually a one-time authorization. After that, you can tell the tool to check that folder for new files on a schedule—hourly, daily, or whenever makes sense for you.

Next, Define Your Data Fields

This is where you play director. It's the most important part of the setup, where you teach the AI what information you actually need from those statements. It’s a lot like showing a new assistant exactly what to look for on a page.

You'll typically upload a sample bank statement and use the software’s interface to visually point out the important fields. You're not building a rigid template; you're just giving the AI examples so it can learn the context and patterns.

For any bank statement, you'll need to identify the essentials:

- Transaction Date: The column showing when each transaction happened.

- Description: The text explaining the transaction (e.g., "TRADER JOES #123," "Client Payment – INV 456").

- Debit/Withdrawal: The column for money leaving the account.

- Credit/Deposit: The column for money coming into the account.

Here's the cool part: Modern AI-driven tools learn from this. Once you identify the 'Date' column on one statement, the system is smart enough to find the date column on future statements from that same bank, even if the layout shifts slightly.

The whole process starts with Optical Character Recognition (OCR), which is just a fancy way of saying the software "reads" the document and turns the picture of the text into actual digital text the computer can understand. This foundational step is what allows the AI to start analyzing and extracting the data you need.

You can learn more about the details behind this in our guide on how to extract data from PDF files: https://bankstatementconvertpdf.com/how-to-extract-data-from-pdf/

Finally, Configure the Excel Output

Once the software knows what to pull, the last step is telling it how to organize that data. This is how you make sure the final Excel spreadsheet is clean, structured, and ready to use—not a messy data dump that you have to spend another hour cleaning up.

A good configuration involves just a few key settings:

- Column Naming: Be specific. Name your Excel headers exactly what you want, like "Transaction_Date," "Vendor," "Amount_Out," and "Amount_In." Consistency is everything for accounting.

- Data Formatting: Make sure dates are in a standard format (like YYYY-MM-DD) and currency fields are properly formatted as numbers. This will save you from a world of headaches in Excel later on.

- File Naming Convention: Set up a smart rule for naming the output files. Something like "BankName_StatementPeriod_Export.xlsx" (e.g., "Chase_October2024_Export.xlsx") will keep your records organized and easy to find.

After you've set all this up, run a test with a few sample statements. Let the software pull the PDFs, extract the data, and generate an Excel file. Check that first output carefully to make sure everything lines up. For a deeper dive into making these kinds of workflows run smoothly, check out this expert guide on automating data entry.

Once you're happy with the test, flip the switch and activate the workflow. Now, every time a new bank statement hits your Google Drive, the system will automatically process it and spit out a perfect Excel sheet. You've just saved yourself hours of mind-numbing work and cut out the risk of human error.

Fine-Tuning Your System for Maximum Accuracy

Getting your automated workflow up and running is a huge win, but the real magic happens in the fine-tuning. An initial setup is just the foundation. Now, it's time to dial in the settings and build a system that moves from just "good enough" to something you can truly trust, day in and day out.

This process is all about building guardrails and feedback loops. You're essentially teaching the software to be skeptical of its own work, which paradoxically leads to much higher confidence in the final output. The goal is to get from a respectable 95% accuracy to over 99%, which is where the real value of automation kicks in.

Implementing Smart Data Validation Rules

One of the most powerful things you can do is set up data validation rules. Think of these as simple, logical checks that automatically flag or reject data that just doesn't make sense. It’s like having a meticulous proofreader built directly into your workflow.

Consider the common errors you'd look for manually. You can program the software to do the same thing, but instantly and without fail.

- Format Checks: Is the 'Date' column actually a date? Set a rule to ensure it only accepts valid formats (like MM/DD/YYYY). Anything else gets flagged.

- Numeric-Only Fields: Columns like 'Debit' and 'Credit' should only contain numbers. A rule here prevents a stray bit of text from a messy OCR scan from throwing off your totals.

- Range Validations: If you know certain transactions should never be negative, a rule can catch when an OCR error accidentally inserts a minus sign.

These rules are your first line of defense. They catch the most obvious mistakes before they ever pollute your final spreadsheet, a fundamental step in making data entry automation reliable.

The real power of an automated system isn't just speed; it's consistency. Data validation rules enforce this consistency at scale, performing checks that a human might forget or overlook, especially after reviewing hundreds of lines of data.

Handling Exceptions and Learning from Corrections

No system is perfect. Eventually, it will encounter a bank statement format it's never seen or a layout that a bank suddenly changed. How your workflow handles these exceptions is what separates a decent setup from a great one.

Modern tools with AI aren’t static; they're designed to learn. When the software flags an entry it's unsure about, your correction does more than just fix that single error. You are actively training the underlying model. For instance, if it misreads a transaction description, your manual fix helps it recognize similar descriptions correctly in the future.

This creates a powerful feedback loop. The more you use the system and correct its rare mistakes, the smarter and more accurate it becomes. This adaptive learning is a key feature to look for in modern financial data extraction tools.

Creating a Human-in-the-Loop Review

For absolute confidence—especially when dealing with sensitive financial data—a 'human-in-the-loop' approach is the gold standard. This doesn't mean manually checking every single line item. That would completely defeat the purpose of automation.

Instead, it’s about a smart, targeted review.

You can configure the system to flag only the entries it has low confidence in. For example, you might set a rule that if the software's confidence score for a particular field dips below 98%, it gets highlighted for a quick human check.

This lets a team member spend a few minutes reviewing a handful of uncertain entries, rather than hours slogging through thousands. It's the perfect blend of machine speed and human oversight, ensuring maximum accuracy without sacrificing the huge time savings you get from automation.

Keeping Your Automation Running Smoothly and Growing With You

Putting an automation system in place isn't the finish line; it’s the starting line. Think of it less like a one-time setup and more like a dynamic tool that needs a bit of care to keep performing at its peak. Once you have your workflow humming along, the real game begins: maintaining it and getting it ready to handle more as your business grows.

A well-organized system is the foundation of it all. You absolutely need a clean, logical trail for every single document. This means setting up a straightforward folder system for your PDFs and the resulting Excel files, maybe breaking them down by month or client. This isn't just about being tidy—it's essential for accounting and makes it a breeze to track down the source of any transaction later.

Keeping an Eye on Performance and Proving Its Worth

To really understand the value your system is providing, you have to measure it. You don’t need fancy tools for this; a simple spreadsheet log will do the trick. The idea is to track a few key metrics to see the real-world impact.

- How Accurate Is It? Every so often, grab a few output files and give them a once-over. Are there any errors? Make a note of them. This simple check helps you quantify the accuracy and shows you if the software needs a bit more guidance on certain types of statements.

- How Much Time Are We Actually Saving? This is your golden metric. Figure out how many hours your team used to burn on manual data entry each month. Compare that to the tiny amount of time spent now just reviewing the output. That difference is your ROI in its purest form.

The goal here is to shift from "I think this is faster" to "We've reclaimed 15 hours of team time this month." Hard numbers like that make it easy to justify expanding automation to other parts of the business.

Taking Your Automation to the Next Level

Once you've nailed bank statements, you've built a solid base. The logical next move is to apply that same thinking to other mind-numbing, document-heavy tasks. The core process of pulling out and organizing data works for all sorts of financial paperwork.

Consider what else you could automate:

- Vendor Invoices: Imagine pulling invoice numbers, due dates, and line items automatically. Your accounts payable process would get a whole lot faster.

- Customer Receipts: Digitize and sort expenses as they come in, making reimbursements and tax time so much easier.

- Purchase Orders: Automatically check incoming invoices against POs to catch any mismatches right away.

The push for this kind of efficiency is huge. The industrial automation market hit around $206 billion in 2024, and for good reason. Automating data entry alone can deliver an ROI between 30% and 200% in the first year. But here's the catch: many of these projects fizzle out because they aren't properly maintained or scaled.

When you start expanding your workflow, you’re effectively building a central data hub for your entire operation. To handle different document types without a headache, it’s worth looking into versatile bank statement extraction software that can learn and adapt. This is how a simple fix for bank statements becomes a cornerstone of your business's efficiency, changing the way you handle data for good.

Have Questions About Automating Data Entry? Let's Talk.

Jumping into an automated system for something as sensitive as financial data naturally brings up some questions. It's smart to get these sorted out before you go all-in. Let's walk through some of the most common things people ask when they're ready to stop typing and start automating their bank statement workflow.

Think of this as the final gut-check—making sure you’re confident this is the right move for your business, your security, and your sanity.

How Secure Is This, Really?

Security is always the first question, and for good reason. Any professional-grade automation tool worth its salt puts security front and center. Most tools handle this in one of two ways: they either process everything locally on your own computer (so your data never even touches the internet) or use robust, end-to-end encryption for cloud-based processing.

Honestly, it's often a huge security upgrade from manual methods. Think about it—no more papers left on a desk, no risk of statements getting lost in a pile, and no unauthorized eyes glancing over someone's shoulder. A good tool keeps everything contained.

When you're vetting software, look for clear privacy policies and check for compliance certifications like SOC 2 or GDPR. A controlled digital environment simply has fewer vulnerabilities than a paper-based one.

Can It Actually Handle All My Different Bank Statements?

Yes, and this is where the technology has gotten incredibly good. Older systems were a nightmare; they relied on rigid templates, so the second a bank tweaked its statement design, the whole process would break.

Today’s smart tools use AI to read and understand a document like a human would. Instead of just looking for data in a specific box on a grid, the software identifies fields like ‘Transaction Date’ or ‘Amount’ by their context. It understands what the data is, not just where it sits on the page.

You might have to do a quick one-time setup to show it what a statement from a new bank looks like, but from there, it learns and adapts. This makes it incredibly reliable for handling statements from all sorts of different banks without needing constant hand-holding.

The real magic of modern AI is its ability to adapt. It’s not about fixed templates anymore; it’s about contextual understanding, which is exactly what you need for the wild world of financial document layouts.

What's This Going to Cost, and Is It Worth It?

Pricing models vary. You’ll find everything from monthly subscriptions for online tools to one-time license fees for desktop software. But the conversation should really be about the return on investment (ROI), which is almost always faster and bigger than people expect.

Here’s a simple way to ballpark it: Figure out how many hours your team spends keying in data each week. Multiply that by their hourly rate, and then tack on a bit more for the time spent finding and fixing the inevitable typos and errors.

Most businesses I've seen find the software pays for itself in just a couple of months. The savings aren't just in labor costs; it's about getting more accurate data and, most importantly, freeing up your team to do analysis and other high-value work instead of mind-numbing transcription. For more on this, it's often helpful to check out a company's frequently asked questions page.

What Happens if the Software Misreads Something?

Let’s be realistic: no OCR (Optical Character Recognition) is perfect 100% of the time. The best automation software is built with this in mind. Instead of just giving you a file and hoping for the best, it includes a validation step.

The software will flag any characters or fields where it has a low confidence score—maybe a smudge on the PDF or a funky font—and present them to you for a quick double-check.

This "human-in-the-loop" approach is the sweet spot. You get the speed of automation for the 99% of data it reads perfectly, combined with the assurance of a human review for that tricky 1%. It’s the most efficient way to get data that’s not just fast, but completely trustworthy.

Ready to eliminate manual data entry for good? With Bank Statement Convert PDF, you can transform your bank statements into clean, organized Excel files in minutes. Start your free trial today and see how much time you can save at https://bankstatementconvertpdf.com.