For many small business owners, 'bookkeeping' is a word that triggers a mix of dread and confusion. It's often seen as a necessary evil, a time-consuming chore that pulls you away from what you love doing: running and growing your business. But what if you could transform bookkeeping from a source of stress into a powerful tool for growth and stability? Effective financial management is the bedrock of a sustainable enterprise. It's not just about compliance; it's about having a clear, real-time understanding of your financial health, enabling you to make smarter, more strategic decisions.

This guide moves beyond generic advice to provide a clear path to financial control. We will break down eight fundamental and actionable small business bookkeeping tips designed for immediate implementation. You will learn how to build a robust system by separating finances, automating key processes like reconciliation, and establishing systematic tracking for both receivables and documentation. Whether you're a new freelancer or an established shop owner, these insights will help you create a financial foundation that saves time, minimizes errors, and gives you the confidence to steer your business toward lasting success. Let's dive into the practical steps that will put you in command of your numbers.

1. Separate Business and Personal Finances

The most foundational of all small business bookkeeping tips is to draw a clear, unwavering line between your business and personal finances. This means more than just having a rough idea of what’s what; it requires establishing separate legal and financial entities for your company. By opening dedicated business bank accounts and credit cards, you create a distinct financial ecosystem for your enterprise.

This separation is not merely an organizational preference; it is a critical practice for legal protection, tax compliance, and accurate financial analysis. When business and personal funds are commingled, it becomes nearly impossible to track your company's true profitability and cash flow. Furthermore, for incorporated businesses like LLCs or corporations, mixing funds can "pierce the corporate veil," putting your personal assets at risk in the event of a lawsuit or business debt.

Why This Separation is Non-Negotiable

Maintaining distinct accounts is essential from day one. It simplifies every subsequent bookkeeping task, from routine expense tracking to year-end tax preparation. A clean, business-only transaction history removes the guesswork and tedious work of manually separating expenses, reducing the risk of costly errors and overlooked deductions.

- Accurate Reporting: It allows for a clear view of your business's financial health, enabling better strategic decisions.

- Tax Compliance: It makes tax time significantly easier and less stressful, as all your business income and expenses are consolidated and easily verifiable.

- Legal Protection: For incorporated entities, it upholds the legal liability shield that separates your personal assets from business obligations.

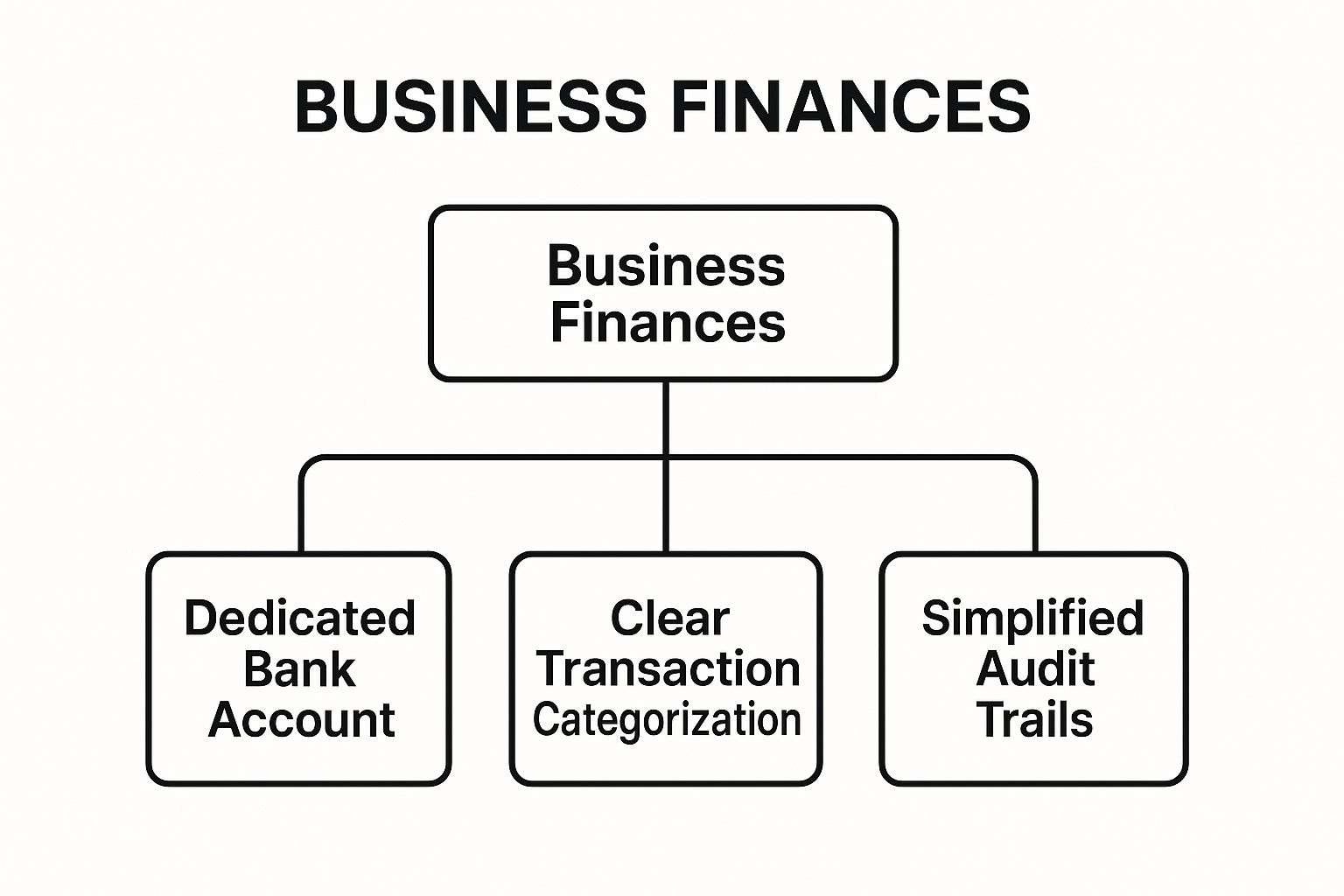

The following infographic illustrates the hierarchy of benefits that stem from this core principle, showing how a dedicated account structure supports clearer transaction management and simplifies financial oversight.

As the diagram highlights, establishing dedicated accounts is the foundational step that directly enables clear transaction categorization and, ultimately, creates a simplified audit trail for your business.

Actionable Steps for Implementation

To put this principle into practice, start by opening a business checking account as soon as you form your company. Direct all revenue into this account and pay all business expenses from it. If you accidentally use a personal card for a business purchase, don't just ignore it. Create a formal expense reimbursement process: submit a receipt to your business and issue a payment from the business account back to your personal account, documenting it as a "reimbursement." This maintains the integrity of your records.

2. Implement a Consistent Chart of Accounts

Once your finances are separated, the next crucial step in building a robust bookkeeping system is to implement a consistent Chart of Accounts (COA). A COA is a comprehensive, organized list of every account in your general ledger, acting as the financial skeleton for your business. It categorizes every single transaction, from revenue earned to expenses paid, providing the structure needed for meaningful financial reporting and analysis.

Creating a well-organized COA is not just an administrative task; it's a strategic one. It allows you to transform raw transaction data into actionable business intelligence. For example, instead of a single vague "Supplies" expense, a construction company might create specific accounts like "Lumber," "Fasteners," and "Safety Gear." This level of detail enables precise job costing and identifies areas where material costs are rising.

Why a Tailored COA is a Game-Changer

A generic, one-size-fits-all COA can obscure critical insights. A customized chart tailored to your specific industry and business model is essential for accurate performance tracking. It provides the foundation for all financial statements, including your Balance Sheet and Income Statement, ensuring they reflect the true nature of your operations. This is one of the most impactful small business bookkeeping tips for gaining clarity on your profitability.

- Granular Analysis: A detailed COA allows you to analyze profitability by service, product line, or department. For instance, a law firm can track revenue and expenses for each practice area (e.g., family law vs. corporate law).

- Budgeting and Forecasting: With clearly defined expense categories, you can create more accurate budgets and forecast future spending with confidence.

- Simplified Tax Preparation: A well-structured COA aligns with tax form categories, making it significantly easier to identify and claim all eligible deductions at year-end.

A thoughtful COA, like those found in accounting software like QuickBooks, brings order to financial chaos. It ensures that every dollar is accounted for and categorized consistently, preventing the confusion that arises from ambiguous or overlapping accounts.

Actionable Steps for Implementation

You don't need to create your COA from scratch. Start with an industry-specific template provided by your accounting software or CPA. Customize it to fit your unique operations. A common best practice is to use a numbering system to organize accounts logically (e.g., 1000s for Assets, 4000s for Income, 6000s for Operating Expenses).

Review your COA quarterly to ensure it still meets your needs. Prune unused accounts and add new ones as your business evolves. Most importantly, document what each account is for and train anyone involved in bookkeeping on its proper use. This consistency is key to generating reliable financial reports that you can use to make smarter business decisions.

3. Automate Recurring Transactions and Bank Reconciliation

Embracing automation is one of the most impactful small business bookkeeping tips for reclaiming valuable time and reducing human error. This involves leveraging technology to handle repetitive financial tasks, such as creating recurring invoices for subscriptions, recording monthly rent payments, or processing loan installments. Modern accounting software excels at this, connecting directly to your business bank accounts and credit cards to automatically import transaction data.

This automation transforms bookkeeping from a tedious data-entry chore into a strategic oversight function. Instead of manually typing in every expense and deposit, your system does the heavy lifting. This not only speeds up the process but also dramatically increases accuracy by eliminating typos and missed entries. For businesses with high transaction volumes, like a retail store processing daily credit card sales or a SaaS company managing hundreds of subscriptions, automation is a game-changer.

Why This Automation is Non-Negotiable

Automating your financial workflows allows you to focus on growing your business rather than getting bogged down in administrative tasks. It provides a real-time view of your financial position, as bank transactions can be synced daily. This timeliness is crucial for making informed decisions about cash flow, budgeting, and spending. It also establishes a consistent, reliable process that isn't dependent on manual effort, ensuring your books are always up-to-date.

- Time Savings: Drastically cuts down on the hours spent on manual data entry and reconciliation.

- Increased Accuracy: Minimizes the risk of human error, leading to more reliable financial records.

- Real-Time Insights: Provides an up-to-the-minute look at your finances for better decision-making.

The following video demonstrates the power of automation in modern accounting and how it simplifies the reconciliation process.

As shown, integrating your bank accounts with your accounting software creates a seamless flow of information that is the cornerstone of efficient bookkeeping.

Actionable Steps for Implementation

Begin by identifying your most frequent and predictable transactions, such as rent, software subscriptions, or utility bills. Set these up as recurring expenses in your accounting software. Next, connect your business bank and credit card accounts to enable automatic bank feeds. To make this even more powerful, create "bank rules" that automatically categorize common transactions. For example, a rule can be set to always classify payments to "Chevron" as "Vehicle: Fuel." While this automates much of the process, it's still wise to review the categorized entries weekly. For those managing complex reconciliations, you can find more information about the process by exploring bank reconciliation on Excel. This ensures any exceptions or miscategorizations are caught and corrected promptly.

4. Track and Digitize All Receipts and Documentation

Proper receipt and document management is a cornerstone of accurate small business bookkeeping. This practice involves more than just stuffing receipts into a shoebox; it requires systematically collecting, organizing, and storing all business-related financial documentation. This includes not just purchase receipts but also invoices, bank statements, supplier contracts, and any other document that substantiates a business transaction.

Transitioning from physical paper to a digital system is crucial for efficiency, security, and compliance. Modern tools allow you to scan and upload documents to the cloud, making them easily searchable and accessible while meeting IRS requirements for record-keeping. A digital system protects you from lost or faded receipts and creates an audit-ready trail that supports every entry in your books.

Why This Diligence is Non-Negotiable

Failing to maintain proper documentation can lead to significant problems, including missed tax deductions, inaccurate financial reports, and major headaches during an audit. Each receipt is proof of a legitimate business expense. Without it, you cannot claim the deduction, potentially leading to a higher tax bill. A disciplined approach ensures every cent is accounted for and properly justified.

- Audit-Proof Records: A complete, digitized set of documents provides irrefutable evidence for every transaction during an IRS or state audit.

- Maximizing Deductions: It guarantees you have the necessary proof to claim every eligible business expense, from office supplies to client meals.

- Enhanced Accuracy: It provides a clear reference for your bookkeeper (or you) to correctly categorize expenses, improving the reliability of your financial statements.

Automating this process with the right software is a game-changer. For instance, tools specializing in bank statement extraction can pull data directly from digital statements, further streamlining the data entry and verification process.

Actionable Steps for Implementation

Creating a robust digital filing system is easier than it sounds. The key is to establish a consistent habit. Use a mobile app like Dext or Expensify to photograph receipts immediately after a purchase; many of these apps integrate directly with accounting software like QuickBooks or Xero. For paper documents you receive at the office, set a weekly time to scan and file them. Organize your cloud storage (like Google Drive or Dropbox) with a simple folder structure, such as "Expenses > 2024 > 10-October," with subfolders for categories like "Supplies," "Travel," and "Utilities."

5. Perform Regular Bank Reconciliation

One of the most crucial small business bookkeeping tips for maintaining financial integrity is to perform regular bank reconciliations. This process involves systematically comparing the transactions recorded in your business's accounting software or ledger with the official statements from your bank and credit card companies. The goal is to ensure that every deposit, withdrawal, and fee matches perfectly, bringing your internal records into alignment with your financial institution's records.

Regular reconciliation is the cornerstone of accurate financial reporting and a powerful defense against errors and fraud. It confirms that the cash balance in your books is correct, which is essential for making sound business decisions. Without it, you might be operating with a flawed understanding of your cash flow, potentially leading to bounced checks, overdraft fees, or missed opportunities. For example, an e-commerce business must reconcile not just its bank account but also its accounts with payment processors like Stripe and PayPal to get a true picture of its cash position.

Why This Practice is a Monthly Necessity

Performing bank reconciliation monthly, rather than quarterly or annually, is non-negotiable for a healthy business. This frequent check-up allows you to catch discrepancies quickly before they snowball into significant problems. A small error, like a transposed number or a missed bank fee, is much easier to investigate and correct when the transaction is still fresh in your mind.

- Error Detection: It helps identify data entry mistakes, duplicate payments, or bank errors promptly.

- Fraud Prevention: Regular review of transactions can uncover unauthorized charges or suspicious activity, allowing you to act immediately.

- Cash Flow Management: It provides a precise, up-to-date picture of your available cash, which is critical for budgeting and planning.

This disciplined monthly routine transforms bookkeeping from a historical record-keeping task into a proactive financial management tool. For a detailed walkthrough, you can find a comprehensive bank reconciliation statement example on bankstatementconvertpdf.com to guide your process.

Actionable Steps for Implementation

To integrate this practice into your workflow, schedule a specific time each month, shortly after receiving your bank statements. Begin with your primary business checking account, as it often has the highest transaction volume. Use your accounting software’s reconciliation feature, which simplifies the process by automatically suggesting matches.

Go line by line, checking off each matching transaction between your books and the bank statement. If you find a discrepancy, investigate it immediately. It could be a check that hasn't cleared yet (a timing difference), a bank service charge you forgot to record, or an error. Make the necessary adjusting entries in your accounting records and add notes explaining the reason for the adjustment. This creates a clear audit trail and ensures your financial reports are always accurate and reliable.

6. Monitor Cash Flow with Regular Financial Reporting

Profitability on paper is not the same as having cash in the bank. This makes regular cash flow monitoring one of the most critical small business bookkeeping tips for survival and growth. This practice involves creating and consistently reviewing financial reports to understand the precise timing of money entering and leaving your business. It goes beyond a simple monthly profit and loss statement, focusing on the real-world movement of funds.

By generating weekly cash flow statements, monthly profit and loss (P&L) reports, and quarterly balance sheets, you can forecast and prevent dangerous cash shortages. For example, a seasonal retail business uses cash flow forecasting to know exactly when to order inventory for its peak season without running out of operating capital. Similarly, a consulting firm can track outstanding invoices and project timelines to predict revenue dips and surges, allowing it to manage expenses accordingly.

Why This Reporting is Non-Negotiable

Consistent financial reporting provides the clarity needed for sound strategic decision-making. It transforms bookkeeping from a historical record into a powerful predictive tool. Without a firm grasp on your cash flow, you might find your business unable to pay suppliers, make payroll, or seize growth opportunities, even while appearing profitable. Regular reporting uncovers trends, highlights inefficiencies, and provides the data needed to steer your business effectively.

- Prevent Cash Crunches: Proactively identify potential shortfalls and arrange for financing or adjust spending before it becomes a crisis.

- Improve Decision-Making: Make informed choices about hiring, inventory purchases, and capital investments based on real-time financial data.

- Track Performance: Gain deep insights into your business's financial health, identifying your most and least profitable service lines or products.

Effective monitoring empowers you to manage your financial resources with precision, ensuring the business remains healthy and resilient. To further streamline this process, you can explore using a bank statement format in Excel to organize raw data for easier analysis.

Actionable Steps for Implementation

Start by building a simple weekly cash flow forecast. List all expected cash inflows (e.g., invoice payments, sales) and all anticipated cash outflows (e.g., payroll, rent, supplier payments) for the coming weeks. Most modern accounting software can automate the generation of key reports like the P&L and balance sheet, so take the time to set these up. Focus on analyzing trends over several periods rather than single-month snapshots to understand the bigger picture. Use these reports to hold yourself and your team accountable for financial targets.

7. Establish a Systematic Accounts Receivable Process

Waiting for customer payments can be one of the most stressful parts of running a small business. Establishing a systematic accounts receivable (AR) process transforms this passive waiting game into an active, controlled workflow. This involves creating standardized procedures for invoicing clients, tracking payments, and professionally managing overdue accounts.

A robust AR system is the engine of your cash flow. Without it, you are essentially providing interest-free loans to your customers with no clear repayment schedule. By defining clear payment terms, sending invoices promptly, and implementing a consistent follow-up protocol, you significantly reduce the time it takes to convert a sale into cash in the bank. This predictability is vital for covering expenses, investing in growth, and maintaining financial stability.

Why a Systematic Approach is Crucial

An ad-hoc approach to invoicing and collections leads to inconsistent cash flow and mounting bad debt. A defined process ensures every customer receives the same professional treatment and that no invoice falls through the cracks. It professionalizes your business operations and sets clear expectations, which can strengthen customer relationships rather than strain them.

- Improved Cash Flow: It accelerates the collection of payments, providing your business with the working capital it needs to operate smoothly.

- Reduced Bad Debt: Proactive follow-ups decrease the likelihood that an invoice becomes an uncollectible write-off.

- Professionalism: A consistent and clear process shows customers you are organized and serious about your financial operations.

A marketing agency that sends invoices with net-30 terms immediately upon project completion is a prime example. They don't wait for the end of the month; the work is done, and the invoice is sent. This simple habit shortens their payment cycle significantly.

Actionable Steps for Implementation

To build your AR process, start by defining your payment terms (e.g., Net 15, Net 30, Due on Receipt) and stating them clearly on all quotes and invoices. Send invoices immediately after delivering a product or completing a service, not weeks later. If an account becomes overdue, initiate a follow-up sequence. For instance, a B2B supplier might implement automated email reminders at 15, 30, and 60 days past due, ensuring consistent communication without manual effort. Consider offering a small discount for early payment to further incentivize promptness.

8. Plan and Prepare for Tax Obligations Year-Round

One of the most impactful small business bookkeeping tips is to treat tax preparation as a year-long activity, not a last-minute scramble. Proactive tax planning involves consistently setting aside funds, tracking deductions, and staying aware of your financial position to meet tax obligations without stress or surprise. This approach transforms tax season from a chaotic event into a predictable, manageable process.

This continuous planning is crucial for managing cash flow and minimizing your tax liability legally. Instead of facing a massive, unexpected tax bill in April, you anticipate your obligations and prepare for them methodically. This strategy not only prevents penalties for underpayment but also allows you to make strategic decisions, like investing in new equipment or contributing to retirement accounts, to optimize your tax outcome.

Why This Proactive Approach is Essential

Integrating tax planning into your monthly bookkeeping routine ensures you are always prepared. It provides a real-time understanding of your potential tax burden, which is vital for accurate financial forecasting and business budgeting. A year-round strategy helps you avoid the cash flow crisis that can cripple a small business when an unplanned tax payment is due.

- Avoid Penalties: Making timely estimated tax payments throughout the year helps you avoid costly IRS penalties for underpayment.

- Maximize Deductions: Consistent tracking ensures you don't miss out on legitimate deductions, from home office expenses to software subscriptions, which can significantly lower your taxable income.

- Improve Cash Flow: By regularly setting aside money for taxes, you prevent a large, single withdrawal from disrupting your operational funds.

For instance, a freelance designer who diligently tracks all software subscriptions, home office expenses, and client-related mileage can claim thousands in deductions. Similarly, a small retail business that makes quarterly estimated payments based on its profits avoids a year-end financial shock and maintains healthy cash reserves.

Actionable Steps for Implementation

To implement this, begin by creating a dedicated savings account specifically for taxes. A common rule of thumb is to transfer 25-30% of every payment or profit into this account. Automating this transfer can make the process seamless. Use your bookkeeping software to tag every potential tax-deductible expense as it occurs, not months later when memory fades.

Consult with a tax professional for strategic planning sessions, not just for filing your return. They can provide guidance on tax law changes and help you identify opportunities, such as establishing a SEP-IRA to reduce your current taxable income while saving for retirement. This forward-looking collaboration is a hallmark of sophisticated financial management.

Small Business Bookkeeping Tips Comparison

| Item | Implementation Complexity 🔄 | Resource Requirements ⚡ | Expected Outcomes 📊 | Ideal Use Cases 💡 | Key Advantages ⭐ |

|---|---|---|---|---|---|

| Separate Business and Personal Finances | Medium – requires discipline and multiple account setups | Moderate – multiple bank accounts, ongoing management | Clear financial separation, simplified tax prep, legal protection | Small business owners, freelancers needing clear audit trails | Reduces IRS risk, preserves corporate veil, simplifies tracking |

| Implement a Consistent Chart of Accounts | Medium to High – needs accounting knowledge and periodic updates | Moderate – setup and staff training | Consistent categorization, accurate reports, better analysis | Businesses requiring detailed financial reporting and tax compliance | Enables scalable, standardized bookkeeping and financial clarity |

| Automate Recurring Transactions and Bank Reconciliation | High – setup and ongoing monitoring needed | High – needs accounting software and reliable tech | Time savings, reduced errors, real-time financial data | Businesses with repetitive transactions and high volume | Improves efficiency, minimizes manual errors, supports cash flow management |

| Track and Digitize All Receipts and Documentation | Medium – requires consistent discipline and tech adoption | Moderate – scanning apps, cloud storage subscriptions | Organized documents, audit readiness, easy retrieval | All businesses needing detailed expense documentation and compliance | Prevents document loss, enables remote access, saves physical space |

| Perform Regular Bank Reconciliation | Medium – time-consuming and detail-oriented | Moderate – accounting knowledge and regular effort | Accurate financial records, fraud detection, error correction | Any business aiming for reliable financial statements and audits | Identifies discrepancies early, ensures statement accuracy, supports compliance |

| Monitor Cash Flow with Regular Financial Reporting | Medium – ongoing data collection and report interpretation | Moderate – accounting software, time investment | Early cash shortage warnings, improved decision-making | Businesses needing cash flow visibility and financial planning | Prevents crises, spots trends, supports vendor/customer management |

| Establish a Systematic Accounts Receivable Process | Medium to High – process creation and customer management needed | Moderate to High – invoicing systems, follow-up resources | Improved cash flow, reduced bad debt, professional collections | Companies with receivables needing timely payments and customer relations | Enhances collections, predicts revenue, professional customer interaction |

| Plan and Prepare for Tax Obligations Year-Round | Medium to High – ongoing tracking and professional advice | Moderate to High – tax software, expert consultations | Lower tax liability, penalty avoidance, improved cash flow | Businesses wanting proactive tax management and deduction maximization | Reduces stress, maximizes deductions, supports year-round compliance |

From Bookkeeping Burden to Business Superpower

Navigating the financial landscape of a small business can often feel like a complex and demanding journey. However, the eight essential bookkeeping tips we've explored provide a clear roadmap to transform this potential burden into one of your greatest business superpowers. By implementing these strategies, you are not just tidying up your records; you are building a resilient, data-driven foundation for sustainable growth and long-term success.

The journey begins with foundational discipline. Separating your business and personal finances is the non-negotiable first step, creating the clarity needed for all subsequent financial activities. From there, establishing a consistent Chart of Accounts provides the structural skeleton for your financial reporting, ensuring every dollar is categorized meaningfully. These initial organizational efforts set the stage for more powerful, efficiency-driving habits.

Weaving Efficiency into Your Financial Fabric

Once your foundation is solid, the focus shifts to creating streamlined, repeatable processes. Automating recurring transactions and embracing software-driven bank reconciliation are game-changers, freeing up valuable time and significantly reducing the risk of manual error. This efficiency is further amplified by a commitment to digitizing every receipt and document, creating an accessible, organized, and audit-proof archive of your financial history.

These practices culminate in the ability to generate and analyze critical financial reports. Regular bank reconciliation, diligent cash flow monitoring, and a systematic approach to accounts receivable are not just chores; they are the very mechanisms that allow you to understand the story your numbers are telling. This is where the true power lies. Instead of reacting to financial surprises, you can proactively make strategic decisions, identify growth opportunities, and mitigate risks before they escalate.

From Reactive Task to Proactive Strategy

Ultimately, the most crucial takeaway from these small business bookkeeping tips is the shift in mindset they encourage. Proactive, year-round tax planning, for instance, transforms tax season from a stressful scramble into a predictable, manageable part of your business cycle. Each of these tips works in concert to move you from a reactive state of "doing the books" to a proactive state of "using your financial intelligence."

Your financial data is more than just a collection of numbers for the tax authorities. It is a real-time dashboard reflecting the health, challenges, and opportunities within your business. Mastering these bookkeeping fundamentals empowers you to read that dashboard with confidence, enabling you to make smarter, more informed decisions that will fuel your company's growth and secure its financial future. Start by implementing one or two of these tips today, build momentum, and watch as financial clarity becomes your strategic advantage.

Struggling to digitize and import transaction data from PDF bank statements? Streamline your bookkeeping with Bank Statement Convert PDF, a powerful tool designed to quickly and accurately convert your PDF statements into clean, usable CSV files. Bank Statement Convert PDF helps you conquer one of the most tedious bookkeeping tasks, making reconciliation faster and more efficient.