Think of forensic accounting as financial detective work. It’s where accounting, auditing, and sharp investigative skills come together to scrutinize financial records, usually in the middle of a legal fight or criminal case. In short, it’s part accountant, part private eye.

What Is a Financial Detective

Picture a crime scene. But instead of dusting for fingerprints, the crucial evidence is buried deep inside spreadsheets, ledgers, and transaction histories. This is the world a forensic accountant operates in—they are the financial detectives brought in to piece together the real story behind the numbers.

They possess all the precision of a traditional accountant but pair it with the healthy skepticism of a seasoned investigator. Their job isn't just about making sure the books balance. It's about following the money, no matter where it leads, to uncover fraud, settle disputes, or simply make sense of a chaotic financial mess.

This kind of deep dive into financial records means every single transaction is under a microscope. One entry can be the thread that unravels an entire scheme. That’s why verifying document authenticity is so critical, and a thorough bank statement verification is often the very first step to build a case on solid ground.

To really grasp what makes them different, it helps to see how they stack up against the accountants most people are familiar with.

Forensic Accountant vs Traditional Accountant A Quick Comparison

While both roles are built on a solid foundation of accounting principles, they operate with completely different goals and mindsets. It’s like the difference between a family doctor and a surgeon—both are medical experts, but they're called in for very different reasons.

This table breaks down the key distinctions.

| Aspect | Traditional Accountant | Forensic Accountant |

|---|---|---|

| Primary Goal | To record, summarize, and report financial transactions accurately. | To investigate financial discrepancies and gather evidence for legal proceedings. |

| Mindset | Compliant and detail-oriented, focused on adherence to standards. | Skeptical and investigative, looking for anomalies and signs of deception. |

| Scope of Work | Broad, covering day-to-day financial operations and reporting. | Narrow and specific, focused on a particular issue like fraud or a legal dispute. |

| Outcome | Financial statements, tax returns, and compliance reports. | Expert reports, litigation support, and courtroom testimony. |

Ultimately, a traditional accountant ensures everything is in its right place, while a forensic accountant comes in when there's a suspicion that things have been deliberately put in the wrong place.

Thinking Like a Detective: The Forensic Accountant's Mindset

To really get what forensic accounting is all about, you have to stop thinking like a regular accountant and start thinking like a detective. It's a shift from just checking the numbers for accuracy to looking at them with a healthy dose of professional skepticism. A forensic accountant's starting point is to assume nothing and question everything. The numbers might tell a story, but is it the true story?

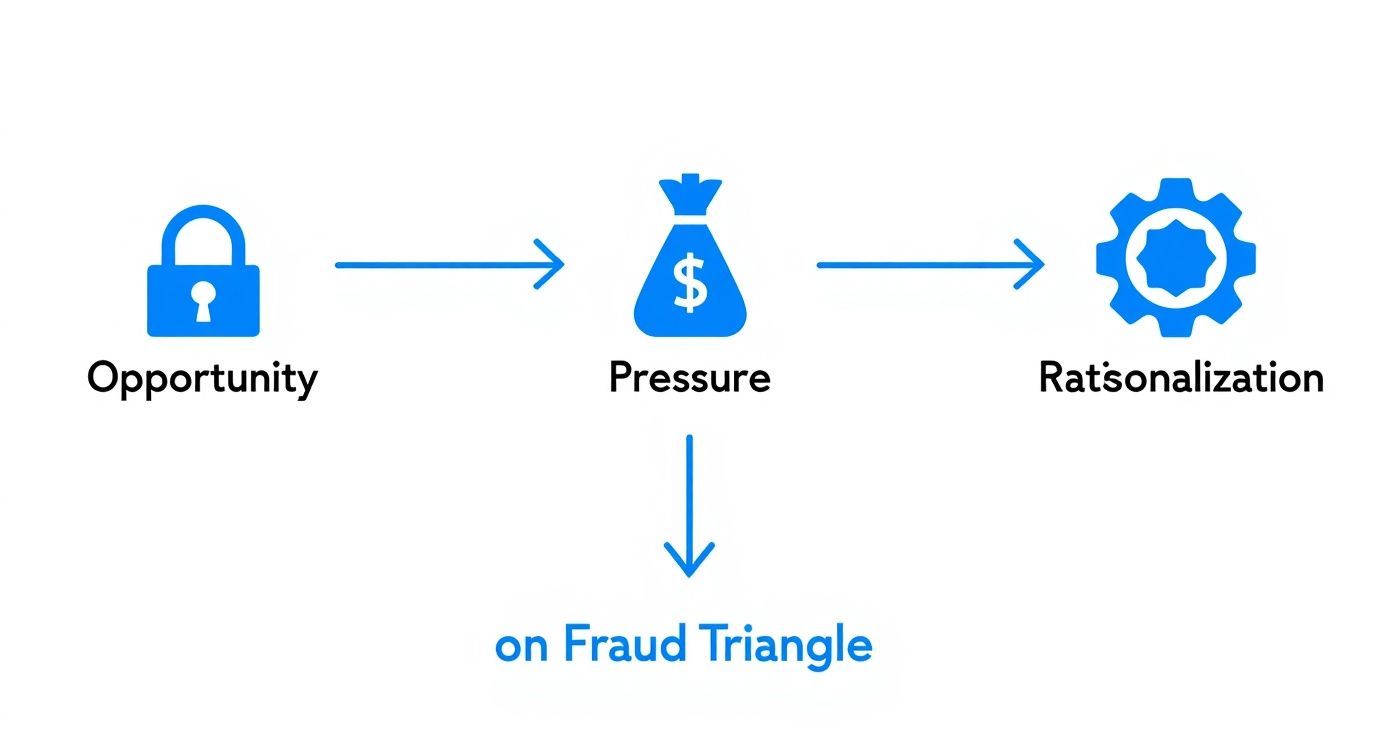

This investigative approach is built on core principles that explain why financial crimes happen in the first place. One of the most powerful frameworks for this is the Fraud Triangle. It breaks down why a seemingly trustworthy person might cross the line.

- Pressure: This is the motive. The person is facing a financial problem they can't solve legitimately. It could be mounting medical bills, gambling debts, or just an insatiable desire for a lifestyle they can't afford.

- Opportunity: This is the means. The person sees a way to commit the fraud with a low chance of getting caught. Think weak internal controls, a lack of oversight, or a position of trust that they can exploit.

- Rationalization: This is the excuse. The fraudster tells themselves a story to justify their actions. "I'm just borrowing the money," or "The company owes it to me," or "No one is getting hurt."

When these three elements click into place, the stage is set for fraud. A huge part of a forensic accountant's job is spotting the red flags tied to each of these points.

Keeping the Evidence Pure

Finding the "smoking gun" is only half the battle. Every piece of evidence a forensic accountant uncovers has to be strong enough to stand up in court. This is where the concept of chain of custody becomes non-negotiable.

From the second a bank statement is collected or a digital file is copied, its journey must be documented obsessively. Who had it? When? Where was it stored? This meticulous log proves the evidence hasn't been tampered with.

A broken chain of custody can get even the most damning evidence thrown out of court. One mistake can torpedo the entire case. This is why the process is so rigid—it protects the integrity of the financial story the evidence tells.

This discipline is what truly sets forensic accounting apart from a standard audit. If you want to dive deeper into the nuts and bolts of examining financial documents, our guide on how to audit financial records explores these meticulous processes in more detail.

Uncovering the Truth with Forensic Audit Techniques

To get to the bottom of financial deception, a forensic accountant needs a unique toolkit. It's a mix of old-school detective work and modern technology, all aimed at one thing: following the money. These techniques are designed to turn a gut feeling into hard evidence that can stand up in court. The process is painstaking, involving everything from digging through public records to interviewing key people.

Bank statements are often ground zero for an investigation. A close look at vendor payments, for instance, can reveal a clever kickback scheme where an employee is using a fake "shell" company to pocket cash. By scrutinizing transaction patterns, dates, and amounts, an investigator can spot red flags that a typical audit would sail right past. We cover these methods in more detail in our guide to financial statement analysis techniques.

A forensic audit isn’t about finding a needle in a haystack. It’s about knowing exactly which piece of hay is most likely to be hiding the needle. The techniques are targeted, efficient, and driven by an investigative hypothesis.

Knowing how fraud happened is only half the battle; you also need to understand why. That's where the Fraud Triangle model comes in.

This infographic breaks down the three conditions that are almost always present when fraud occurs: Opportunity, Pressure, and Rationalization.

As you can see, for someone to commit fraud, they usually need a motive (Pressure), a weakness in the system to exploit (Opportunity), and a personal justification for their actions (Rationalization).

The High-Tech Side of the Investigation

These days, forensic accounting is about much more than paper ledgers. Investigators now use data analytics and digital forensics software to churn through millions of electronic files in a fraction of the time it used to take. These tools can automatically flag suspicious keywords in emails, spot altered digital documents, and even recover deleted files that hold the smoking gun. This tech-heavy approach is absolutely critical for cracking today's complex, digital fraud schemes.

Artificial intelligence and machine learning have taken things even further, giving investigators a serious edge. AI algorithms can scan massive datasets to find anomalies and patterns a human could never spot on their own. This makes investigations faster and more accurate, but the human expert is still essential for putting the digital clues into context. You can explore more about these advancements reshaping forensic accounting practices.

When to Call in a Forensic Accountant

Think of a forensic accountant as a financial detective. You don't need them for your day-to-day bookkeeping, but when the numbers don't add up and there's a suspicion of foul play, they are the experts you call in.

Their job is to follow the money, untangling complex financial webs to get to the truth. Knowing when to bring them on board can mean the difference between a quick resolution and a long, expensive battle.

High-Stakes Financial Scenarios

Certain situations are practically tailor-made for a forensic accountant's skillset. These are the moments when a standard audit just won't cut it because you need to go far deeper than the surface-level numbers.

Here are a few classic examples where their expertise is invaluable:

- Corporate Fraud Investigations: A company suspects an executive is embezzling funds or that the books have been cooked. A forensic accountant is brought in to dig through the records, pinpoint the fraud, calculate the exact amount of the loss, and package the evidence for legal action.

- Complex Divorce Cases: In messy divorces, especially with high-net-worth individuals, one spouse might be hiding assets. Forensic accountants are hired to trace every dollar and provide a true valuation of the marital estate, ensuring a fair split.

- Partnership Disputes: When business partners are at odds, it’s often over money. If one partner suspects the other is secretly funneling cash out of the company, a forensic accountant can provide an objective, third-party analysis to settle the matter.

These cases often involve deliberate deception, including falsified documents. Our guide on how to spot fake bank statements can give you an idea of the kinds of red flags they look for.

A forensic accountant’s real magic isn't just finding the numbers; it's telling the story behind them. They translate dense financial data into a clear, compelling narrative that a judge, jury, or lawyer can easily understand.

The demand for these financial investigators is booming for a reason. Valued at roughly $7.2 billion in 2025, the forensic accounting market is expected to climb to nearly $12.8 billion by 2032. This growth is a direct response to the rising tide of financial crime and the critical need for experts who can expose it.

Why Forensic Accounting Is More Important Than Ever

In a world where business is increasingly digital and regulatory scrutiny is at an all-time high, the need for financial truth-seekers is booming. Forensic accounting has shifted from a small, specialized field into a cornerstone of modern business, largely driven by a perfect storm of rising fraud and a relentless demand for transparency.

Today's digital transactions create endless avenues for complex financial crimes. This, coupled with the fallout from major corporate scandals, has put organizations under immense pressure to keep their books clean and prove their integrity to everyone from investors to the public.

The Impact of Regulation and Market Growth

Legislation like the Sarbanes-Oxley Act (SOX) completely reshaped the corporate governance landscape. Passed in the wake of huge accounting scandals, SOX mandated stricter internal controls and financial reporting, making forensic skills indispensable for any company serious about compliance.

This shift isn't just a trend; it's a fundamental change backed by hard numbers. The need for experts who can navigate this complex environment has turned forensic accounting into an economic powerhouse.

The market valuation tells the story. The global forensic accounting sector was valued at around $20.08 billion in 2025 and is expected to grow at a compound annual rate of 7.7%. This growth is fueled directly by the rising tide of corporate fraud and the non-negotiable demand for accountability. You can explore more data on forensic accounting market trends.

Ultimately, forensic accountants have become the guardians of financial integrity. Their work is essential for building the trust that a healthy economy relies on, ensuring the numbers we see aren't just accurate, but true.

Your Questions About Forensic Accounting Answered

Diving into forensic accounting usually sparks a lot of curiosity about the job itself, the techniques involved, and where it all fits in the real world. It's so much more than crunching numbers; it’s a career that demands a sharp mind and a unique set of skills.

Let's break down some of the most common questions people have about this fascinating field.

How Do You Become a Forensic Accountant?

The path usually begins with a solid education, like a bachelor’s degree in accounting. From there, most people go on to earn their Certified Public Accountant (CPA) license, which is really the cornerstone of a serious accounting career.

But to really dig into the investigative side of things, you need to go a step further. Aspiring financial detectives often pick up specialized credentials to prove they have what it takes.

- Certified in Financial Forensics (CFF): This one really hones in on your experience and expertise specifically within forensic accounting.

- Certified Fraud Examiner (CFE): This is a globally respected certification that shows you're skilled in spotting, stopping, and investigating fraud.

Of course, it’s not just about the certifications. You need an intensely analytical mind, a knack for spotting tiny details others miss, and the ability to clearly explain your findings, whether you're interviewing a witness or testifying in court.

What Is the Difference Between a Forensic Audit and a Regular Audit?

Think of a regular audit like a routine health check-up. The goal is to get a general overview of a company’s financial health and make sure the statements are reasonably accurate. It's preventative, not diagnostic.

A forensic audit is completely different. It's what happens when you call in a specialist because you suspect something is seriously wrong.

Instead of a broad review, it’s a targeted investigation, usually triggered by a suspicion of fraud, embezzlement, or some other kind of financial crime. The main goal is to gather solid evidence that will hold up in court.

What Happens After a Forensic Accountant Finds Fraud?

When the investigation wraps up, the forensic accountant puts together a comprehensive report. This document lays out everything: what they found, how they found it, and all the evidence to back it up.

This report goes to the client—maybe the company’s leadership or its lawyers. From there, a few things can happen:

- The company might take internal disciplinary action.

- An insurance claim could be filed to get the stolen money back.

- The findings might become the basis for a civil lawsuit or even criminal charges.

It's also common for the forensic accountant to be called as an expert witness. Their job is to take complex financial information and explain it to a judge and jury in a way that’s easy for everyone to understand.

When an investigation means digging through stacks of financial records, the right tools make all the difference. For professionals who need to quickly pull data from PDF bank statements, Bank Statement Convert PDF is a game-changer. Our software turns messy bank statement PDFs into clean, organized Excel files, saving you countless hours of manual data entry. Learn how to automate your data extraction process today.