At its heart, the bank reconciliation formula is a straightforward calculation. Its job is to make sure the cash balance you have recorded in your company's books lines up perfectly with the cash balance shown on your bank statement.

The formula bridges the gap between these two records by accounting for transactions that one side knows about but the other doesn't yet. Think of things like outstanding checks you've written but haven't been cashed, or deposits in transit you've made that haven't cleared the bank.

What Is the Bank Reconciliation Formula

Imagine your company’s accounting records and your bank statement as two people telling the same story from slightly different perspectives. They’re both talking about your cash, but timing differences almost always mean their stories don't match up exactly at the end of the month.

The bank reconciliation formula acts as the bridge between these two narratives. It provides a structured method to identify and account for these discrepancies, ultimately leading to a single, verified cash amount. This is often called the "true" or "adjusted" cash balance.

It’s really not so different from balancing your personal checkbook against your mobile banking app. You know you wrote that rent check for $1,500, but until your landlord cashes it, your banking app thinks you have $1,500 more than you actually do. The reconciliation formula just applies this same logic in a more formal way for a business.

The Two Core Formulas

To get your books and the bank statement to agree, you actually work with two formulas, not just one. You start at opposite ends—one formula for the bank's balance and another for your book balance—and make specific adjustments to each. The end goal is simple: both formulas must arrive at the exact same number.

This process is designed to align your company’s internal cash records with the bank statement balance. The main adjustments usually involve adding deposits that are still in transit and subtracting checks that are still outstanding from the bank’s balance. You can dive deeper into how these adjustments align financial records on the Solvexia blog.

Adjusted Bank Balance = Bank Statement Balance + Deposits in Transit – Outstanding Checks ± Bank Errors

Adjusted Book Balance = Company Book Balance + Bank Credits (e.g., Interest) – Bank Debits (e.g., Fees) ± Company Errors

To get a handle on these formulas, it helps to break down exactly what each component means.

Key Terms in the Bank Reconciliation Formula

Here’s a quick reference table breaking down the essential components you'll need to master the bank reconciliation formula.

| Component | What It Represents | Common Impact on Balance |

|---|---|---|

| Bank Statement Balance | The ending cash balance shown on your official bank statement. | This is your starting point for the bank-side calculation. |

| Deposits in Transit | Cash or checks you've recorded as received but haven't yet cleared the bank. | Increases the bank balance. |

| Outstanding Checks | Checks you've written and recorded that have not yet been cashed by the recipient. | Decreases the bank balance. |

| Company Book Balance | The ending cash balance according to your internal accounting records (e.g., your general ledger). | This is your starting point for the book-side calculation. |

| Bank Credits | Money the bank added to your account that you may not have recorded yet (e.g., interest earned). | Increases your book balance. |

| Bank Debits | Money the bank deducted from your account that you may not have recorded yet (e.g., monthly service fees). | Decreases your book balance. |

| Errors | Mistakes made by either you or the bank that need correction. | Can either increase or decrease the relevant balance. |

Understanding these terms is the first step. Once you're comfortable with what each piece represents, you can confidently apply the formulas to reconcile any set of books.

Breaking Down Each Part of the Formula

To really get a handle on the bank reconciliation formula, you have to understand the story behind each number. These aren't just figures on a page; they represent real-world events that create a temporary gap between what your books say and what the bank statement shows.

Let's pull apart the key players in this process.

Adjustments to the Bank Balance

First, we'll look at the adjustments made to the ending balance on your bank statement. These are almost always about timing—transactions you’ve already recorded, but the bank just hasn't caught up with yet.

-

Deposits in Transit: Picture this: you deposit a customer's check late on the last day of the month. You've already logged that cash into your system, but it won't show up on your bank statement until it officially clears, which is often the next business day. This amount is added back to the bank's balance because, from your perspective, that money is already yours.

-

Outstanding Checks: This is the reverse. You write and mail a check to a supplier on June 29th and immediately deduct it from your cash balance. But that supplier might not deposit it until July 5th. Until they do, the bank thinks you have more money than you actually do. These checks are subtracted from the bank balance to account for the payments that are guaranteed to come out.

Adjustments to Your Book Balance

Now, let's flip the script. The second set of adjustments covers things the bank knows about, but you haven't recorded yet. These are the little surprises you usually discover when you first look at the monthly statement.

Think of these as financial "notes" left by your bank. You have to update your own records to account for them, making sure your book balance reflects reality. This is all about correcting your own ledger, not the bank's.

You'll need to scan your statement for a few common items:

-

Bank Service Charges: These are the pesky monthly maintenance fees, wire transfer costs, or other charges the bank automatically deducts. You’ll need to subtract these from your book balance.

-

Interest Earned: On the bright side, if you have an interest-bearing account, the bank deposits this income for you. You must add this interest to your book balance to properly record the new cash.

-

Notes Collected: Sometimes, a bank might collect a payment on your behalf (like a loan you made to someone else) and deposit it straight into your account. This is another addition to your book balance.

By carefully spotting and applying these adjustments, you bring two different starting points—the bank's and yours—into perfect alignment. It's a systematic approach that transforms a confusing mismatch into a single, reliable cash figure you can trust.

Putting The Formula To Work With A Real Example

Theory is one thing, but seeing the bank reconciliation formula in action is where it all starts to make sense. Let's walk through a practical example for a fictional small business, "Creative Designs," to see how all the pieces fit together.

First, we need the right documents for the month ending June 30th. For Creative Designs, that means grabbing their latest bank statement and their internal cash ledger.

- The Bank Statement shows an ending balance of $12,500.

- The company's Cash Ledger (their books) shows an ending balance of $11,890.

Right away, you can see the numbers don't match. Don't panic—this is completely normal. Our job is to use the formula to figure out why and get them to agree.

Calculating The Adjusted Bank Balance

We'll start with the bank's side of things. We need to adjust the bank's balance for transactions that Creative Designs knows about, but the bank hasn't processed yet. After comparing the cash ledger to the bank statement, a couple of items pop out.

First, a deposit of $1,800 made on June 30th hasn't appeared on the statement yet. This is a classic deposit in transit. Second, two checks written in June still haven't been cashed: Check #1205 for $650 and Check #1208 for $320. These are our outstanding checks.

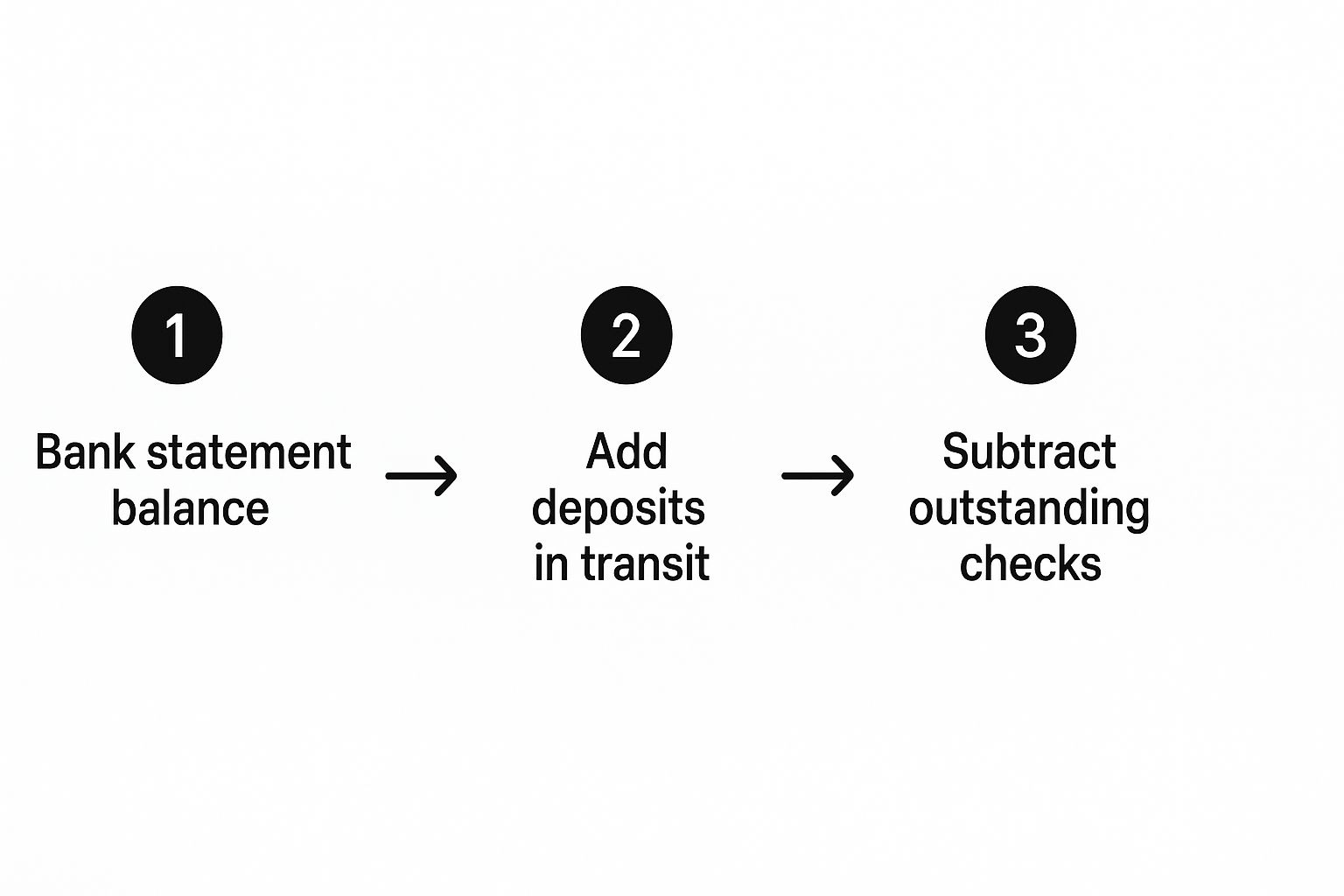

Here’s a simple visual that breaks down how we adjust the bank's numbers.

This shows how we start with the bank’s figure, apply our adjustments, and get closer to the true cash position.

Adjusted Bank Balance Calculation:

- Start with Bank Balance: $12,500

- Add Deposits in Transit: + $1,800

- Subtract Outstanding Checks: – $970 ($650 + $320)

- Final Adjusted Bank Balance = $13,330

Calculating The Adjusted Book Balance

Now, let's flip over to the company's books. We need to adjust Creative Designs' cash balance for items the bank knows about, but the company hasn't recorded yet.

A quick scan of the bank statement reveals a few things: the company earned $25 in interest (nice!), a customer paid a $1,500 invoice directly via an electronic transfer, the bank charged a $35 monthly service fee, and a customer's check for $50 bounced (an NSF check). If you want to dive deeper, you can explore a complete bank reconciliation statement example on our site.

Let's plug these into our book balance:

Adjusted Book Balance Calculation:

- Start with Book Balance: $11,890

- Add Interest Earned: + $25

- Add Customer Payment: + $1,500

- Subtract Service Fee: – $35

- Subtract NSF Check: – $50

- Final Adjusted Book Balance = $13,330

And just like that, we have a match! Both the adjusted bank balance and the adjusted book balance equal $13,330. The accounts are officially reconciled, giving Creative Designs an accurate picture of its true cash position.

Sample Bank Reconciliation Walkthrough

This side-by-side table shows the final calculations from our example, clearly demonstrating how both the bank and book balances are adjusted to arrive at the same reconciled amount.

| Bank Side Adjustments | Amount | Book Side Adjustments | Amount |

|---|---|---|---|

| Ending Bank Balance | $12,500 | Ending Book Balance | $11,890 |

| Add: Deposits in Transit | $1,800 | Add: Interest Earned | $25 |

| Add: Customer Payment | $1,500 | ||

| Less: Outstanding Checks | ($970) | Less: Bank Service Fee | ($35) |

| Less: NSF Check | ($50) | ||

| Adjusted Bank Balance | $13,330 | Adjusted Book Balance | $13,330 |

Seeing both sides meet at the same final number is the ultimate goal of any bank reconciliation.

Finding and Fixing Common Reconciliation Discrepancies

Sooner or later, you'll hit a wall. You’ve followed the formula perfectly, but the final numbers just don't line up. Don't panic. This happens to everyone, and it's a completely normal part of reconciling your accounts.

The good news is that most discrepancies aren't signs of a major financial disaster. They’re usually small, simple things—a timing issue, a forgotten fee, or a minor typo. The trick is knowing where to look and how to hunt down the culprit without wasting hours.

Think of it less like a crisis and more like solving a puzzle. Let's walk through where to start your search.

Your Troubleshooting Checklist

When your adjusted balances don’t match, run through this list. I always start with the most common slip-ups first because, more often than not, the fix is quick and easy.

-

Simple Math Errors: Before you dive into the deep end, just double-check your math. It sounds obvious, but you’d be surprised how often a simple addition or subtraction mistake is the root of the problem.

-

Transposed or Slide Errors: This is a classic accounting blunder. Did you type $54 instead of $45? That’s a transposition. Or maybe you entered $50.00 when you meant $500.00? That’s a slide error. Here’s a neat trick: if the difference between your balances is divisible by 9, you almost certainly have a transposed number somewhere.

-

Forgetting to Record Bank Fees: It’s so easy to miss these. Scan your bank statement one more time for that $15 monthly service charge or a $30 wire transfer fee. Those little debits need to be subtracted from your company’s book balance.

-

Missing Interest or Credits: On the flip side, did the bank pay you interest? Make sure you’ve added any interest earned or other automatic credits to your book balance.

Finding an error doesn’t mean you messed up. It means the reconciliation process is doing its job—catching small issues before they become big ones and ensuring your financial records are accurate.

Deeper Investigation Tactics

If the usual suspects aren't to blame, it's time to dig a little deeper. A very common issue is an outstanding check or deposit from a previous reconciliation that finally cleared the bank this month. Pull out last month's reconciliation and compare your list of outstanding items against this month's bank statement.

For a more structured approach, a good worksheet is your best friend. It keeps everything organized and makes it much harder to miss a step. If you don't have one, this bank reconciliation statement template is a great place to start. It guides you through the process, helping you track every adjustment and see exactly where the numbers went off track.

How Technology Is Changing Bank Reconciliation

While it's crucial to understand the bank reconciliation formula, the tools we use to apply it have changed dramatically. Thankfully, the days of manually ticking off transactions on a paper ledger against a physical bank statement are mostly behind us. That process was incredibly slow and, frankly, a breeding ground for human error, turning the month-end close into a task everyone dreaded.

The arrival of spreadsheets in the 1980s felt like a huge leap forward, bringing some basic automation to the calculations and data organization. But today's tools are in a different league entirely. We've moved into an era of fully automated solutions that do most of the heavy lifting. This new wave of technology, often incorporating AI and machine learning, makes real-time reconciliation not just possible, but practical.

This isn't just about saving a few hours. It’s about completely rethinking the entire reconciliation process.

Beyond Speed: The Benefits of Automation

Modern automated bank reconciliation software does so much more than just run the formula faster. These platforms often plug directly into your bank feeds, pulling in transactions as they happen. Smart algorithms then get to work, suggesting matches with a high degree of accuracy. It turns reconciliation from a once-a-month headache into a continuous, dynamic process, giving you a live look at your cash position.

Automation fundamentally strengthens financial controls by creating a clear, unchangeable audit trail. It also goes a long way in reducing the risk of internal fraud by flagging unusual activity and helping separate the duties of recording transactions from approving the final reconciliation.

Ultimately, this shift in technology frees up finance professionals to do more valuable work. Instead of getting bogged down in matching hundreds of line items, they can focus their expertise on investigating genuine discrepancies, analyzing cash flow patterns, and contributing to strategic financial decisions.

Knowing the formula inside and out is what gives you the power to properly manage these tools and make sense of the insights they provide. It ensures your financial foundation is as solid as ever, even as the technology gets smarter.

Common Questions About Bank Reconciliation

Even once you get the hang of the bank reconciliation formula, questions always pop up when you're in the middle of the process. Getting a straight answer can be the difference between a quick monthly task and a major headache.

Let's walk through a few of the most common questions I hear from business owners and bookkeepers. This should help clear things up and get you ready for those real-world situations.

How Often Should My Business Reconcile Its Bank Account?

For most businesses, monthly is the sweet spot. It lines up perfectly with when your bank sends out your statement, so you can get into a regular, predictable rhythm. Doing it once a month is frequent enough to spot weird transactions or bank errors before they spiral out of control.

Now, if you're running a business with a ton of daily transactions—like a busy retail store or restaurant—you might want to reconcile weekly. This gives you a much tighter grip on your cash position and a real-time view of what's happening. If you want to dig deeper into this, our guide on effective cash flow management for small business is a great resource.

What if My Adjusted Balances Still Don't Match?

When the numbers just won't line up, don't panic. The first thing to do is simply re-check your math. It’s the most common reason for a mismatch and, thankfully, the easiest to fix. If the math is solid, go back and carefully review your bank statement and cash book for anything you might have missed.

Here's an old accounting trick: if the difference between your two balances is divisible by 9, you've likely got a transposition error. That means you probably typed something like $81 instead of $18. It's a surprisingly common mistake.

Still stuck? Take a look at last month's reconciliation. It's possible an outstanding check or deposit from the previous period finally cleared this month and is throwing things off.

Does Accounting Software Make This Formula Obsolete?

Not a chance. Modern accounting software is a fantastic tool that automates a ton of the grunt work, like pulling in bank feeds and matching transactions. But it doesn't make the underlying formula irrelevant. In fact, understanding the why behind the reconciliation is more crucial than ever.

Think of it this way: the software does the heavy lifting, but you are still the one who needs to review the final report, look into any discrepancies the system flags, and give it the final sign-off. Knowing the formula helps you understand what the software is actually doing. It gives you the power to spot subtle issues or strange patterns that an algorithm might overlook, ensuring your books are truly accurate.

At Bank Statement Convert PDF, our goal is to simplify your financial data management. Our software is designed to quickly turn your PDF bank statements into clean, organized Excel spreadsheets, saving you hours of time and eliminating manual data entry mistakes. Learn more about how our tool can help you today!