If you're a small business owner, you've probably heard the term "internal controls" and immediately pictured a mountain of red tape better suited for a Fortune 500 company. But let's ditch that idea. At its core, an internal control is simply a policy, procedure, or system you create to protect what you’ve built.

Think of them as the guardrails on the highway of your business. They keep you on the road, prevent costly pile-ups, and ensure you reach your destination safely. These controls are all about minimizing errors, catching fraud before it happens, and making sure your financial data tells the real story.

What Are Internal Controls and Why They Matter

Far from being bureaucratic, internal controls for small businesses are just common-sense security for your money, your data, and your day-to-day work. This isn't about micromanaging or showing you don't trust your team. It’s about building a stable, predictable framework where everyone knows the game plan.

When you get them right, these simple processes become the foundation of a resilient business. They give you the peace of mind to stop worrying about what could go wrong and start focusing on growth.

The Core Purpose of Business Controls

So, what are these controls actually trying to accomplish? It all boils down to giving you "reasonable assurance"—moving you from just hoping things are going well to knowing they are. The goals are straightforward but incredibly powerful:

- Safeguard Your Assets: This is about more than just cash in the register. It’s about protecting your inventory from theft, your customer data from breaches, and your intellectual property from misuse.

- Ensure Accurate Financial Reporting: To make smart decisions, get a loan, or even just file your taxes, you need numbers you can count on. Controls are what make your financial statements trustworthy.

- Promote Operational Efficiency: Good processes eliminate wasted time and effort. They prevent two people from doing the same job and make everyday tasks run like a well-oiled machine.

- Encourage Compliance: Every business has to follow rules, from industry regulations to labor laws. Controls help you stay on the right side of the law and avoid nasty fines.

An effective system of internal controls is crucial because it helps organizations identify and correct errors before they cause costly reputational or financial damage. It transforms reactive problem-solving into proactive risk management.

Moving Beyond Trust

Many small business owners say, "I trust my employees, so I don't need strict controls." That's a great starting point, but it misses the bigger picture. Trust is essential, but internal controls are there to protect everyone—the business and the employees.

A good system creates a transparent environment where honest mistakes are caught and fixed quickly, and clear procedures shield staff from unfair suspicion if something goes wrong.

For example, requiring two signatures on any check over $1,000 doesn't say you think the first person is a thief. It just provides a second set of eyes to catch a typo or a miscalculation. It protects the check-writer by sharing the accountability for that transaction. Ultimately, controls aren't about limiting your people; they're about empowering your business to run securely so it can grow successfully.

The Real Cost of Weak Controls in Small Businesses

It’s easy for a small business owner to think, "Fraud? That won't happen to me. We're too small to be a target." But the hard truth is, your size doesn't make you invisible—it makes you vulnerable. When you're busy wearing every hat in the company, overlooking internal controls isn't just a minor slip-up; it's like leaving the front door wide open for financial and reputational disaster.

The consequences aren't some abstract risk you can ignore. They're tangible, often devastating, events that can bring a growing company to its knees. Without clear systems in place, you create blind spots where theft and mistakes can go unnoticed for months, or even years.

Common Fraud Schemes That Prey on Small Businesses

To build a strong defense, you first need to know what you're up against. Fraudsters count on the fact that you're juggling a dozen different roles, which almost always leaves gaps in financial oversight.

Here are a few of the most common ways they exploit weak controls:

- Employee Embezzlement: This is when a trusted employee steals money. It can be as simple as pocketing cash from the register or as sneaky as creating a fake employee in the payroll system and sending "their" salary to a personal bank account.

- Fake Invoice Scams: Someone—either an employee or an outsider—submits a bogus invoice for goods you never ordered or services you never received. If you don’t have a proper approval process, that invoice gets paid, and the money vanishes.

- Payroll Manipulation: An employee with payroll access might pad their hours, give themselves an unauthorized raise, or, as mentioned, invent a "ghost employee." This is a huge risk when one person handles everything from time tracking to cutting checks.

- Check Tampering: This classic scheme involves altering a real check, forging a signature, or creating a counterfeit one from scratch. A lack of dual signature requirements or regular bank statement reviews makes this incredibly easy to pull off.

These schemes all thrive in one kind of environment: where a single person has too much control over money. The absence of simple checks and balances is your single biggest vulnerability.

The Staggering Financial Impact

The financial hit from fraud can be a knockout blow. Small businesses are especially susceptible, with the median loss for companies under 100 employees hitting $141,000 per incident. That's a massive figure for any small enterprise, often representing the difference between a profitable year and closing up shop for good.

Why so high? Because small companies rarely have dedicated compliance staff, making them juicy targets. The good news is that implementing simple anti-fraud measures—like management reviews and surprise spot-checks—can slash both the financial loss and the duration of a fraud scheme by at least 50%.

"Internal controls aren't about mistrusting your people. They're about protecting your business and your honest employees from the consequences of human error and deliberate fraud. They create a system where doing the right thing is the easiest path."

But the damage goes far beyond the money that was stolen. You'll also face the staggering cost of forensic accountants to figure out what happened, legal fees to go after the culprit, and the priceless time and energy you'll have to divert from growing your business to cleaning up the mess. Taking the time to learn how to audit financial records can be your first and most crucial line of defense.

Beyond the Bottom Line: Reputational Damage

Perhaps the most damaging cost of weak controls is the hit to your reputation. When news of fraud gets out, it shatters the trust you’ve built with customers, suppliers, and even your bank.

A reputation for being poorly managed or financially shaky is incredibly hard to shake. It can make it tougher to get a loan, attract top talent, or win new contracts. That perception of risk can hang over your company for years, acting as a constant drag on your growth.

Ultimately, investing in internal controls for small businesses isn't just another expense—it’s a fundamental investment in your company’s survival, stability, and future success.

Understanding the Three Pillars of Internal Controls

Internal controls can seem like a dense, complicated topic. But once you break them down, they're much easier to grasp. The best way to think about them is as a three-layered security system for your business.

Each layer has a specific job. Together, they form a rock-solid defense against the errors, waste, and even fraud that can sink a small business. This framework, built on preventive, detective, and corrective controls, helps you move from just reacting to problems to actively stopping them before they start.

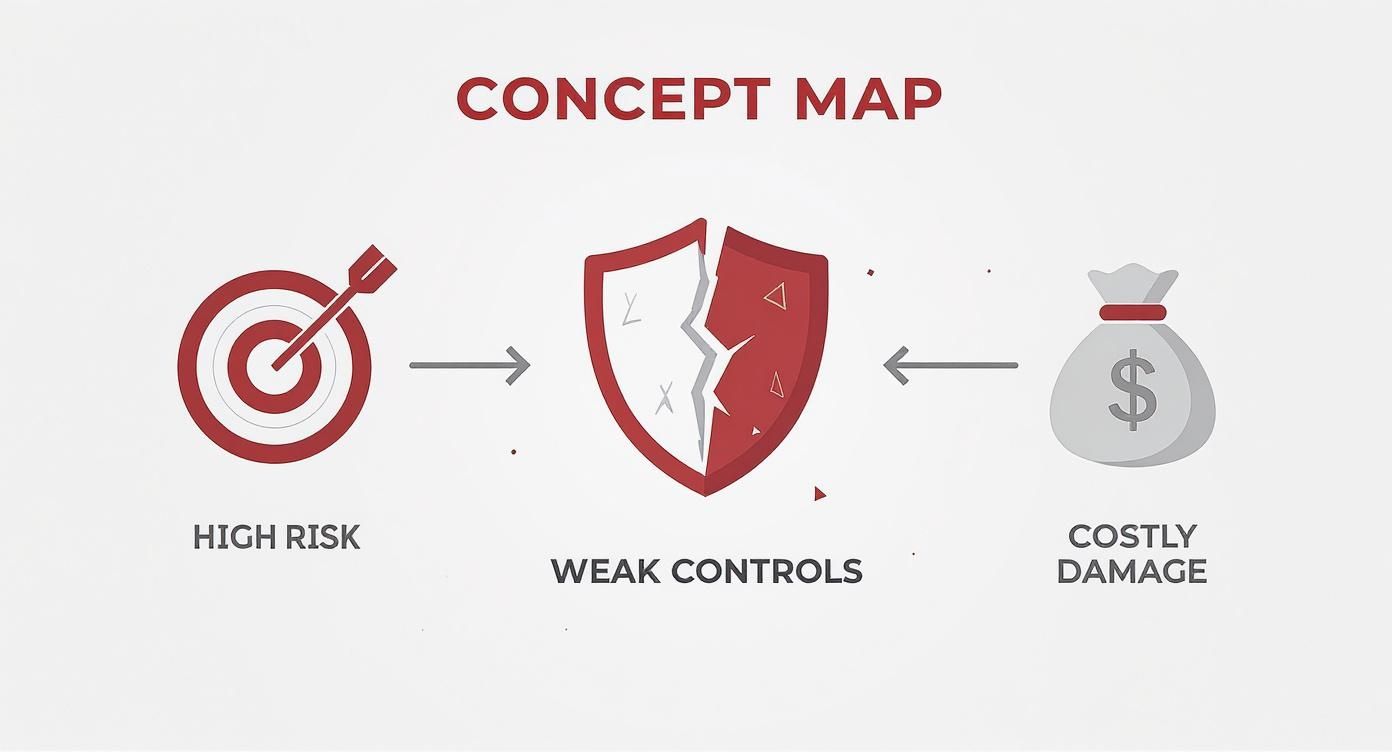

This visual shows exactly what happens when those controls are weak—it creates a high-risk environment that almost always leads to expensive damage.

As you can see, a breakdown in controls is the core vulnerability. It's what opens the door to bigger threats and serious financial consequences.

Pillar 1: Preventive Controls

Think of preventive controls as your first line of defense. Their entire purpose is to stop bad things from happening in the first place. It’s like locking the doors to your shop before a thief even gets to the street. They are proactive, commonsense measures designed to block problems at the source.

In your business, these controls are the rules and procedures you weave into your daily operations. They’re often the most cost-effective because they stop damage before it ever occurs.

A few classic examples include:

- Segregation of Duties: This is a big one. It simply means making sure no single person controls an entire financial process from start to finish. For example, the employee who approves new vendors shouldn't also be the one who pays their invoices.

- Access Restrictions: This is all about limiting who can get to your most valuable assets, both physical and digital. Only trusted staff should have keys to the stockroom or the password to your QuickBooks file.

- Pre-Authorization of Transactions: This requires a manager's sign-off for any significant purchase before the money is spent. It’s a simple check that keeps spending in line with your budget and prevents rogue purchases.

Pillar 2: Detective Controls

Of course, no system is foolproof. That’s where your detective controls come into play. These are your alarm systems and security cameras—they're designed to spot and report on problems after they've already happened. The goal is to catch issues fast, before they spiral out of control.

Detective controls are your safety net, catching the problems that slip past your preventive measures. They also give you critical feedback, showing you where your frontline defenses might be weak.

Here are a few powerful detective controls any small business can use:

- Bank Reconciliations: At the end of every month, sit down and compare your company's cash records against your actual bank statement. This simple habit will instantly flag unauthorized withdrawals, missing deposits, or bank errors.

- Physical Inventory Counts: Don’t just trust what the computer says. Regularly get out on the floor and count your inventory by hand. If the physical count doesn't match your records, you know you have a problem—whether it’s theft, damage, or just sloppy bookkeeping.

- Management Reviews: Make it a habit to regularly review your key financial reports, especially comparing your budget to your actual spending. A sudden, massive spike in office supply costs, for instance, is a red flag that something is wrong.

To make the distinction clearer, here's a quick comparison of these first two types of controls.

Preventive vs. Detective Controls Examples

| Control Type | Objective | Small Business Example |

|---|---|---|

| Preventive | Stop errors or fraud from occurring. | Requiring two signatures on checks over $1,000. |

| Detective | Find errors or fraud after they occur. | Reviewing the monthly canceled check log for unusual payments. |

| Preventive | Reduce the risk of unauthorized access. | Using strong, unique passwords for all financial software. |

| Detective | Identify unauthorized access attempts. | Reviewing system access logs for logins at odd hours or from unknown locations. |

| Preventive | Ensure all purchases are approved. | Requiring a manager's signature on all purchase orders before they are sent. |

| Detective | Verify that recorded assets exist. | Conducting a surprise physical count of high-value inventory items. |

This table shows how both types of controls work hand-in-hand to protect your business's assets and financial integrity.

Pillar 3: Corrective Controls

So, what happens when a detective control sounds the alarm? You need a plan to fix the immediate problem and ensure it never happens again. That’s the job of corrective controls.

Think of these as your emergency response plan. They address the root cause of the issue, not just the symptom. For example, if a surprise inventory count reveals missing items, the corrective control isn't just about writing off the loss. It’s about investigating why it happened, updating your records, and maybe installing a new security camera (a new preventive control) to make sure it's not an easy target next time.

These controls are all about learning from your mistakes. They create a loop of continuous improvement, which is at the very heart of building a resilient and secure business.

How to Implement Essential Internal Controls

Alright, let's move from theory to action. This is where the real value of internal controls starts to shine. The good news? You don’t need a massive budget or a full-time compliance officer to get started. It’s all about putting a few smart, high-impact processes in place to create a safety net for your business.

The secret is to start small and zero in on your biggest risks. You’d be surprised how much protection you can get from a few simple, consistent habits.

Tackle Segregation of Duties

If you do only one thing, make it this. The most powerful internal control for any small business is segregation of duties. The logic is beautifully simple: make sure no single person controls a financial transaction from beginning to end. Just by doing that, you've built an automatic system of checks and balances.

I know what you're thinking. "I only have one person managing the books, how can I possibly segregate their duties?" It's a common hurdle, but the solution is creative oversight from you, the owner.

Here’s how you make it work, even with a tiny team:

- Divide and Conquer: The employee who writes checks or pays bills should never be the one who reconciles the bank account. Period.

- Owner Review is Key: Let your bookkeeper handle the day-to-day transactions. But at the end of the month, you must be the one to personally review and sign off on the bank reconciliation.

- Split Cash Handling: If you run a retail shop or any business with a cash drawer, have one employee count the cash and a different employee prepare the bank deposit.

This approach guarantees a second set of eyes on everything, which drastically cuts down the opportunity for both honest mistakes and deliberate wrongdoing.

Establish Clear Authorization and Approval Workflows

Next up, you need to set clear rules for how money is spent. An authorization workflow is just a fancy term for a system that stops unauthorized spending and keeps expenses aligned with your budget. It’s a critical gatekeeper that adds a layer of accountability before cash ever leaves your business.

Without this, you're flying blind. You open yourself up to budget blowouts, wasteful spending, and even payments to completely fake vendors.

A documented approval process isn't about micromanagement; it’s about creating financial discipline. It ensures every dollar spent is intentional, reviewed, and aligned with your company’s strategic objectives.

Put these simple rules into practice:

- Set Spending Thresholds: Decide on a number, say $500. Any purchase over that amount requires written approval from a manager or the owner before the money is spent.

- Require Purchase Orders: For larger buys, use a basic purchase order system. This creates a neat paper trail connecting the approved request, the invoice, and the final payment.

- Review Vendor Lists: Once a quarter, you or a manager should scan your list of approved vendors. This simple check helps you spot any unfamiliar names that could be part of an invoice scam.

Secure Your Physical and Digital Assets

Protecting your assets means more than just locking the front door. You need to control access to everything from the inventory in the backroom to the data in your accounting software. The guiding principle is simple: grant access only on a "need-to-know" basis.

For your physical assets, this looks like:

- Locking up valuable inventory and keeping a simple log of who holds the keys.

- Keeping blank checks and company credit cards secured in a locked drawer or safe.

And for your digital assets, the same logic applies:

- Use strong, unique passwords for all financial software and make a habit of changing them.

- Dig into your accounting software's settings and create user permissions. The person sending invoices doesn't need to see payroll information.

Make Regular Reconciliations Non-Negotiable

Finally, we arrive at your most powerful detective control: regular reconciliations. This is simply the act of comparing your books to outside statements, like your monthly bank statement. It is your single best tool for catching problems before they spiral out of control.

You need to reconcile every key account at least once a month. Think of it less as a chore and more as a vital health check for your business. For instance, you can elevate your financial oversight by adopting these 8 essential bank reconciliation tips.

This process confirms that the numbers on your screen match reality. Nailing this is a cornerstone of sound financial management. For more on this, our guide on the bookkeeping basics for small business is a great place to start. Remember, it's the consistency that transforms these individual actions into a powerful, protective system.

Using Technology to Strengthen Your Controls

Putting strong internal controls in place used to feel like a big-company game, requiring a hefty budget and a dedicated compliance department. That’s just not the case anymore. For small businesses, affordable technology has completely changed the landscape, bringing enterprise-level security and oversight within reach for everyone. Modern tools can handle the tedious stuff, enforce your rules without fail, and create a clear digital paper trail for every single transaction.

Think of technology as a force multiplier for your controls. It's on the job 24/7, and it doesn't get tired, distracted, or make the kinds of simple mistakes that are all too human. This lets you supercharge your protective measures, giving you a level of oversight that was once reserved for massive corporations.

Automate Your Financial Oversight

The best place to start is right where your money lives: your accounting software. Today's cloud-based platforms are built with strong internal controls baked right in. They aren't just digital ledgers; they're active security systems for your finances.

Many of the best accounting software for small business options come packed with features that automate critical controls:

- User Permissions: You can give employees access only to the functions they need for their job. For instance, your sales team can create invoices, but they can't touch payroll or approve their own expenses.

- Audit Trails: The system automatically logs every action, creating a permanent record of who did what and when. If a number looks odd, you can trace it back to the source in seconds.

- Automated Bank Feeds: By connecting directly to your bank, the software pulls in every transaction automatically. This slashes the risk of manual data entry errors and makes bank reconciliations a breeze.

Lock Down Expense and Payroll Management

Beyond your main accounting hub, specialized apps can help you secure two of the riskiest areas for any small business: employee expenses and payroll. These tools are built from the ground up to enforce your policies automatically.

Expense management apps, for example, let you set spending limits and block certain purchase categories. An employee just snaps a photo of a receipt, and the app processes the claim, checking it against your rules before it ever lands on your desk for final approval. It stops out-of-policy spending before it even starts.

In the same way, dedicated payroll systems create a vital separation of duties. They handle all the complex calculations, tax withholdings, and direct deposits inside a secure platform, drastically reducing the chances for someone to tamper with hours or pay rates.

The pressure is on for businesses of all sizes to tighten up their oversight. In fact, 92% of companies now conduct at least two internal audits annually. Technology is what makes this possible for smaller players, with affordable cloud-based tools enabling the real-time monitoring needed to stay compliant and secure.

Achieving More with Less

At the end of the day, technology allows a small business to build an internal control framework that is both powerful and practical. By automating key preventive and detective controls, you massively reduce your risk of fraud and error without bogging down your operations. This frees you up to focus your time and energy on what really matters—growing your business with the confidence that you have a secure foundation holding everything together.

Building a Culture of Integrity and Control

Rules, processes, and software are powerful, but they only go so far. The most resilient internal controls for small businesses aren't just written down in a dusty manual; they’re woven into the very fabric of your company culture. A strong culture of integrity is your most effective first line of defense.

This shift has to start at the top. When leadership consistently models ethical behavior, it sends a clear and powerful message to the entire team. This "tone at the top" isn't about what you say—it's about making honest, transparent decisions, especially when it's tough.

Set Clear Expectations with a Code of Conduct

A formal code of conduct is the cornerstone that translates your company’s values into clear, actionable guidelines. It needs to be simple, easy to understand, and cover the real-world situations your team might face.

This document shouldn't read like a legal textbook. Think of it more as a practical guide that plainly states your expectations for:

- Honesty and Integrity: Emphasizing the non-negotiable importance of accurate records and truthful communication.

- Conflict of Interest: Clearly defining what a conflict looks like and the exact steps an employee should take to disclose one.

- Confidentiality: Outlining the responsibility every team member has to protect sensitive company and customer information.

Before you can build a culture where controls thrive, you need a clear picture of your current workplace dynamics. A thorough organizational culture assessment is the perfect tool for this.

Empower Your Team with Training and Reporting

A strong culture isn't just a top-down mandate; it's about empowering your employees to become active participants in protecting the business. This boils down to two key things: education and a safe way to speak up.

Provide practical, ongoing fraud awareness training. Help your team understand common schemes and recognize the red flags. The most important part is explaining the "why" behind your controls, so they see them not as burdensome rules but as essential tools to protect their workplace and their jobs. The goal is to give your staff the knowledge to spot suspicious activity—a core concept in financial investigations. You can learn more about what is forensic accounting in our detailed guide on the topic.

Creating a secure, confidential channel for employees to report concerns without fear of retaliation is non-negotiable. Whether it's a simple suggestion box, a designated manager, or an anonymous email address, this empowers your team to become guardians of the business's integrity.

When your team truly understands the mission and feels safe raising concerns, they stop being passive observers and become active stewards of the company’s health.

Common Questions About Internal Controls

Even after seeing how internal controls work, it's completely normal to have a few nagging questions. I see it all the time with small business owners. You're about to introduce new processes, and a little hesitation is natural. Let's walk through the most common concerns I hear to clear things up.

Probably the biggest worry is about the price tag. Many entrepreneurs assume that building a solid system of internal controls for small businesses will break the bank. This is one of the most persistent myths out there, and it holds too many people back.

Are Internal Controls Too Expensive For My Business?

Absolutely not. Let me be clear: effective controls are built on smart processes, not pricey software or a big compliance department. You can put incredibly powerful, low-cost measures in place right now.

For instance, having the owner simply review the monthly bank reconciliation prepared by a bookkeeper costs nothing. Yet, that one action adds a massive layer of oversight. It's all about scalability. Start with simple, foundational habits and only add more complex tools as your business grows and really needs them.

Another hang-up I often see comes down to trust. It sounds something like this: "But I trust my employees completely. Why do I need all these extra rules?" While that sentiment comes from a good place, it misses the entire point of internal controls.

Internal controls aren't about mistrust. They're about creating a predictable, transparent system that protects both the business and its honest employees. Good processes protect your team from unfair suspicion if a mistake happens and simply make it easier for everyone to do their job correctly.

Think of it like a safety net. It’s not there because you expect someone to fall; it's there to catch honest mistakes and, more importantly, to remove the opportunity for things to go wrong. That is the single most effective way to prevent fraud. You're building a system with clear accountability, and that benefits everyone.

Where Is The Best Place to Start?

Feeling a bit overwhelmed? That’s okay. The key is to not try and do everything at once. You don’t need to roll out a dozen new controls overnight. Instead, just focus on a few high-impact steps you can take today.

Here’s a simple game plan to get you started:

- Segregate a Key Duty: Pick one critical financial task, like paying bills. Right now, split the job of preparing payments from the job of approving and signing them.

- Review Your Bank Statement: This one is non-negotiable. As the owner, make it a monthly ritual to personally review the bank statement and the final reconciliation.

- Secure Your Assets: Take one simple action. Move your blank checks into a locked drawer. Create separate, permission-based logins for your accounting software. It's that easy.

Taking these small, deliberate steps is how you start building a stronger, more secure foundation for your business.

Ready to take control of your financial data? Bank Statement Convert PDF provides the tools you need to easily convert your bank statements into Excel, making reconciliations and financial analysis faster than ever. Visit us at https://bankstatementconvertpdf.com to learn more.