The year-end close is that final, critical process where a business double-checks and adjusts all its account balances to prepare the annual financial reports. It’s a comprehensive review of every ledger account, making sure every transaction lands in the right fiscal period before closing out the books for the year.

Building Your Foundation for a Flawless Close

Anyone who's been through a chaotic year-end close knows it feels like a mad dash to the finish line. But the truth is, a smooth process isn't about last-minute heroics; it's built on a solid foundation of preparation laid months in advance. Ditch the generic checklists and focus on creating a framework that fits your business's unique rhythm.

The first step is a realistic, detailed timeline. Don't just grab a template online. Instead, map out key dates and milestones that account for your company's transaction volume and complexity. This customized schedule becomes your roadmap, keeping everyone aligned and preventing that all-too-common year-end scramble.

To help you get started, here's a look at how you might structure your preparatory tasks in the final quarter.

Key Year End Preparation Tasks and Timelines

| Timing (Relative to Year End) | Task | Objective | Responsible Team/Person |

|---|---|---|---|

| 3 Months Out (e.g., October) | Review Fixed Assets & Depreciation | Identify any assets sold or disposed of during the year and update depreciation schedules. | Staff Accountant |

| 2 Months Out (e.g., November) | Vendor & Customer Info Audit | Verify W-9s are on file for all vendors and update customer contact information for year-end statements. | AP/AR Clerk |

| 1 Month Out (e.g., December) | Preliminary P&L and Balance Sheet Review | Run preliminary reports to spot unusual variances or potential misclassifications early. | Controller/Finance Manager |

| Final Week of Fiscal Year | Physical Inventory Count | Conduct a physical count of inventory to reconcile with perpetual inventory records. | Operations & Accounting |

This table is just a starting point, but it illustrates how breaking down the process into manageable, time-bound tasks can transform the year-end from a single, overwhelming event into a controlled process.

Assign Clear Ownership to Prevent Bottlenecks

One of the most common failure points I see in the closing process is ambiguous responsibility. When tasks don't have a clear owner, critical items inevitably fall through the cracks. The fix is simple: assign a specific person to each step on your closing checklist.

This fosters a culture of accountability. For example, your staff accountant is tasked with reconciling all bank and credit card accounts. Meanwhile, the accounts payable clerk is responsible for ensuring all vendor invoices for the period have been received and recorded. This clear division of labor stops duplicate work and ensures no task gets left behind.

Key Takeaway: A successful year-end close isn't a one-person show. It's a coordinated team effort where every member understands their specific contribution to creating the final, accurate financial picture.

This proactive approach is a core principle of good financial management. To build these habits into your daily routine, take a look at our comprehensive guide on the fundamentals of bookkeeping basics for small business.

Choose a Strategic Fiscal Year End

Many businesses just default to a December 31 fiscal year-end, but that’s not always the best move. Your fiscal year should ideally align with your natural business cycle.

For a retail company, closing the books on January 31 often makes more sense. It allows the entire holiday sales season—including post-holiday returns and gift card redemptions—to be captured in a single fiscal year. This strategic choice can dramatically simplify inventory counts and give a much more accurate snapshot of annual performance.

While approximately 70% of public companies use December 31, it's far from a universal standard. Your industry and business model should guide your decision.

Centralize Your Financial Documents

Disorganized documents are the arch-nemesis of an efficient close. Nothing wastes more time than hunting for missing receipts, invoices, or bank statements at the last minute. This frantic search not only causes delays but also introduces a huge risk of inaccurate data.

The solution is to establish a centralized digital system for all financial records before you're in the year-end crunch.

Use a cloud storage solution or a dedicated document management system to create a single source of truth that your whole finance team can access. Get into the habit: when a vendor invoice arrives, it’s immediately scanned and filed. When a bank statement is ready, it’s downloaded and saved to the right folder. This simple discipline turns the year-end close from a chaotic scavenger hunt into a structured, methodical review.

Making Sure the Numbers Match: Reconciliations and Account Verification

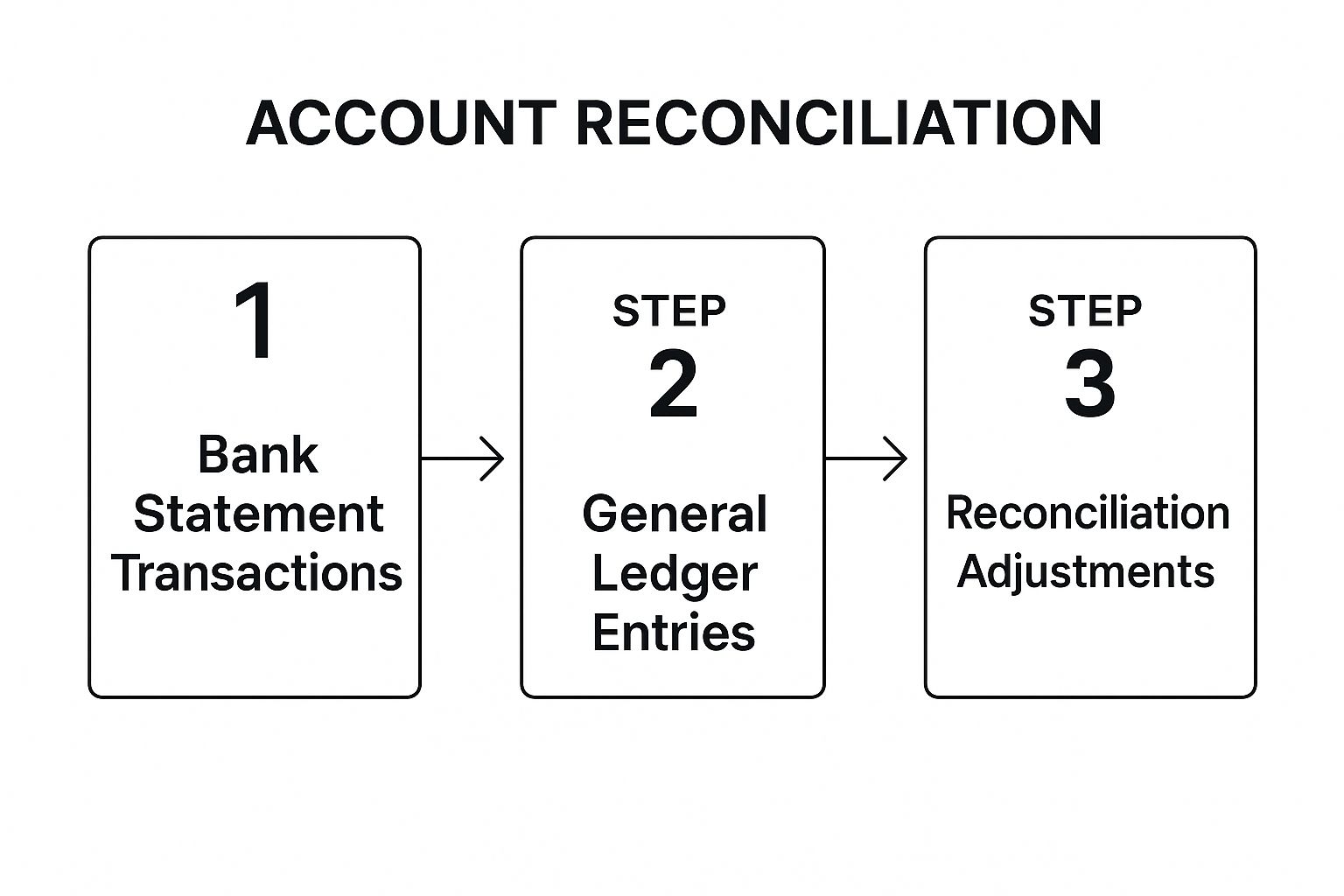

Think of reconciliation as the moment of truth in your year end closing procedures. It’s where the rubber meets the road—the critical step where you meticulously match every single transaction in your general ledger against external documents, like bank statements, to make sure everything lines up. This process is what turns a list of numbers into a credible, defensible story of your company's financial year.

The goal is pretty straightforward: make sure the money you think you have, spent, and received actually matches what the banks and other third parties say. Even a tiny discrepancy is a loose thread you need to pull on and resolve before you can confidently close the books.

This chart gives you a high-level view of how that reconciliation process flows, from external statements through your internal records to the final, adjusted numbers.

As you can see, it's a systematic funnel, filtering all your transaction data through verification to arrive at accurate final balances.

Tackling Bank and Credit Card Reconciliations

The bank reconciliation is the most fundamental piece of this puzzle, yet it’s often where things get bogged down. Getting the year-end close done efficiently is a huge challenge for most businesses. In fact, only about 28% of organizations have managed to automate their financial reporting. This means that for over 80% of companies, manual work is still causing significant delays.

One of the most common headaches I see is dealing with bank statements that come in as PDF files. Manually typing hundreds of transaction lines into a spreadsheet is not just mind-numbingly dull; it's a breeding ground for human error. A single transposed digit can send you down a rabbit hole for hours, searching for a tiny mismatch.

This is exactly where a bit of modern technology can save you a world of pain. Software that can convert those locked PDF bank statements into a usable format like Excel practically eliminates data entry mistakes. You can suddenly sort, filter, and compare your transactions against your books in minutes instead of hours.

Here's what a typical bank reconciliation summary looks like once you've ironed out the differences.

This summary clearly lays out the common reconciling items—like outstanding checks or deposits still in transit—that explain why your bank balance and book balance don't match perfectly at first glance.

Verifying Who Owes You and Who You Owe

Once your cash is squared away, it’s time to look at your accounts receivable (A/R) and accounts payable (A/P). These balances represent the money your customers owe you and the money you owe your suppliers. They're just as important as the cash in the bank.

For A/R, you'll start by running an aged receivables report. This report is your best friend here, as it breaks down all outstanding customer invoices by how long they've been unpaid (e.g., 0-30 days, 31-60 days, and so on). With this report in hand, your mission is to:

- Confirm every invoice on that list is real and was actually sent.

- Flag overdue accounts and kick off the collections process.

- Make the tough call to write off any debts you know you'll never collect.

The process for A/P is similar. You'll run an aged payables report to ensure you've accounted for every bill from your vendors for goods and services you received during the year. It's surprisingly easy to miss a big invoice from late December, which can seriously understate your expenses and make your profit look artificially high.

My Pro Tip: Don't just trust the report. I always recommend picking up the phone and calling customers with large outstanding balances to confirm they agree with the amount. This simple, proactive step can uncover billing disputes or communication breakdowns long before they become a massive year-end headache.

A Real-World Example: The Inventory Count

Let's walk through a common scenario. Imagine a small e-commerce shop that sells custom coffee mugs. All year, they’ve been tracking their inventory in their accounting software. At year-end, they do a physical count and find 1,000 mugs on the shelves. But when they check the software, it says they should have 1,050.

That 50-mug discrepancy might not sound like a big deal, but its effect ripples through the financial statements:

- Cost of Goods Sold (COGS): The value of those 50 missing mugs (at, say, $5 each, that's $250) has to be accounted for. It gets recorded as an expense, increasing COGS and reducing the company's gross profit.

- Inventory Asset Value: The inventory value on the balance sheet is now overstated by $250 and needs to be adjusted down.

- Net Income: With a lower profit, the company's net income and, consequently, its retained earnings will also decrease.

If they skip this adjustment, their profitability and asset base are both wrong. This is precisely why a physical inventory count and reconciliation are absolutely non-negotiable. If you want to get deeper into the mechanics, we've put together a comprehensive guide on account reconciliation best practices.

Finalizing Other Key Accounts

Finally, you need to turn your attention to the other important accounts on your balance sheet. Don't let these slip through the cracks.

- Fixed Assets: Pull up your fixed asset schedule. Go through it line by line to confirm everything listed is still in use, record any disposals from the year, and, most importantly, calculate and book the correct annual depreciation expense.

- Prepaid Expenses: Look at items you paid for upfront, like insurance or annual software licenses. You need to verify the balances and make sure you've expensed the correct portion for the year that just ended.

- Loans and Accrued Interest: Reconcile your loan balances against the statements from your lender. Double-check that you've properly accrued for any interest expense that's been incurred but hasn't been paid yet.

Making Adjusting Entries to Finalize Your Trial Balance

Once your accounts are all reconciled, you’re ready to dive into one of the most important parts of the year end closing procedures: posting adjusting journal entries. This isn't about fixing errors you found earlier. Instead, it’s about making sure your books reflect the reality of when business actually happened, a core principle of accrual accounting.

Think of it this way: you're ensuring that revenue is recognized when it was earned and expenses are recorded when they were incurred, not just when cash finally moves. This step is what makes your financial statements a true and fair picture of your company's performance for the year.

Recording Accrued Expenses and Revenues

Accruals are probably the most common adjusting entries you'll make. They handle the loose ends—the revenue you’ve earned but haven’t invoiced yet, or the expenses you've racked up but haven't been billed for.

-

Accrued Expenses: These are costs your business has already benefited from, but the invoice hasn't hit your desk by year-end. A classic example is employee payroll. If your fiscal year ends December 31 but your next payday is January 5, you have to accrue the wages your team earned during those last days of December. That expense belongs in the old year, not the new one.

-

Accrued Revenue: This is the other side of the coin. Let's say your consulting firm wraps up a big project on December 28th, but you don't actually send the invoice until the first week of January. You earned that money in December, so you need an adjusting entry to record it in the proper period.

Getting these accruals right is what prevents your profits from being over or understated. It’s all about timing.

Handling Prepayments and Deferrals

Next up are prepayments and deferrals. These adjustments deal with situations where cash has changed hands, but the actual service or product will be delivered over time. At year-end, your job is to figure out how much has been "used up."

A perfect real-world example is your annual software subscription. Imagine you paid $1,200 on July 1st for a one-year license. On that day, you recorded the full amount as a prepaid expense, which sits on your balance sheet as an asset.

By December 31st, six months have passed. You've used half of that subscription. So, you need to make an adjusting entry to:

- Decrease your Prepaid Expense asset account by $600 (that’s 6 months x $100 per month).

- Record a $600 Software Expense for the period.

This simple entry ensures your expenses are correctly stated for the year, and the remaining $600 stays on the balance sheet as an asset for the next year. The same logic applies to deferred revenue—when a customer pays you upfront for work you'll do later.

Key Takeaway: Adjusting entries are the workhorse of the matching principle. They make sure that every dollar of revenue is matched with the expenses that helped generate it, all within the same accounting period.

Don't Forget Depreciation

Another adjusting entry you absolutely can't skip is depreciation. This is simply the process of spreading the cost of a physical asset, like a company truck or a new server, over its useful life. It’s a non-cash expense that reflects the wear and tear or obsolescence of your assets.

Figuring out the right amount involves knowing how to calculate depreciation based on the asset's cost, useful life, and salvage value. Booking this expense is essential for presenting accurate asset values and, ultimately, your correct net income.

Running the Adjusted Trial Balance

With all your adjusting entries posted, the next step is to run an adjusted trial balance. This is a fresh report that shows all your account balances after those crucial adjustments have been recorded.

This is your final quality control check. The first thing you'll look for is whether debits still equal credits. If they don't, you know immediately that a mistake was made in one of your entries, and you'll have to do some digging before you can proceed.

The adjusted trial balance is the definitive source of truth for creating your financial statements. To see how these numbers translate into your final reports, check out our guide on building a https://bankstatementconvertpdf.com/financial-statement-in-excel/. Before you do, give that adjusted trial balance one last scan for any accounts with strange-looking balances—this is your last chance to catch an anomaly before closing the books for good.

Closing Your Books and Preparing Financial Statements

Alright, you’ve wrestled with the reconciliations and nailed down all the adjusting entries. Now for the final leg of the journey: closing the books. This is where you formally draw a line under the fiscal year and produce the official reports that tell your company’s financial story.

The first real step here is to close out all your temporary accounts. Think of your revenue, expense, and dividend accounts as buckets that collect data for just one year. To get ready for the next year, you need to empty them.

This is done by rolling their balances into a permanent equity account—almost always Retained Earnings. This one move zeroes out the income statement accounts, effectively hitting the reset button so they can start fresh on day one of the new fiscal year.

The Final Closing Entries

The process for closing temporary accounts is pretty straightforward, but it’s a critical part of the year end closing procedures. These entries lock in your net income and update your company's overall equity.

It usually breaks down into a few key journal entries:

- Close Revenue Accounts: Debit each revenue account for its balance, and credit the total to a temporary holding account often called "Income Summary."

- Close Expense Accounts: Credit each expense account for its balance, and debit the total to that same Income Summary account.

- Close the Income Summary Account: The balance left in the Income Summary account is your net income (or loss). Now, you transfer this final number to Retained Earnings.

- Close Dividend Accounts: If you paid dividends, you’ll credit the Dividends account to zero it out, debiting Retained Earnings directly.

After you post these, every single one of your revenue and expense accounts should have a zero balance.

Generating Your Core Financial Statements

With your adjusted trial balance finalized, you have everything you need to build the three cornerstone financial statements. These documents are the entire point of the year-end close, giving a clear, standardized look at your company’s health.

The numbers come directly from your adjusted trial balance. It's really just a matter of pulling the right balances and slotting them into the correct report format.

A Quick Tip from Experience: Before you start building the reports, give your adjusted trial balance one last look. Do a quick scan for any account balances that just feel… off. It’s your last chance to catch a mistake before it gets cemented into your official financials.

The Income Statement: Your Profitability Story

First up is the Income Statement, which you might also know as the Profit and Loss (P&L) statement. This report is all about performance over time—in this case, the entire fiscal year you just closed.

It’s built on a simple formula: Revenue – Expenses = Net Income. You’ll list all your revenue at the top, subtract the Cost of Goods Sold (COGS) to get your gross profit, and then list out all your operating expenses to land on your net income or loss. This is the bottom line that tells you if the business actually made money.

The Balance Sheet: A Snapshot in Time

Next, you’ll put together the Balance Sheet. Unlike the income statement, which covers a whole year, the balance sheet is a snapshot of your company’s finances on a single day: the very last day of your fiscal year.

It's all about the fundamental accounting equation: Assets = Liabilities + Equity. One side lists everything the company owns (assets), and the other lists everything it owes (liabilities and equity). This statement shows the financial structure and stability of your business. All the numbers are pulled directly from your finalized adjusted trial balance.

The Statement of Cash Flows: Tracking the Cash

Finally, you'll prepare the Statement of Cash Flows. This one is incredibly important because it shows exactly how cash moved through your business. It’s the bridge that connects the net income from your P&L with the actual cash balance on your balance sheet.

This report breaks down all cash movement into three activities:

- Operating Activities: Cash from your main day-to-day business operations.

- Investing Activities: Cash used to buy or sell long-term assets, like equipment or property.

- Financing Activities: Cash from investors or banks, or cash paid out to shareholders.

These three statements have to tell a consistent story. The net income from the P&L flows into retained earnings on the balance sheet, and the statement of cash flows explains the change in your cash balance from last year’s balance sheet to this year's. Reviewing them together is the final sanity check for your entire year-end close.

Using Technology to Make Your Closing Process Easier

Let's be honest: relying on paper stacks and manual spreadsheets for your year-end closing procedures is a recipe for burnout and costly mistakes. Technology isn't just a "nice-to-have" anymore; it's essential for any modern finance team. The right tools can turn your close from a dreaded marathon into a smooth, controlled process.

The move to digital finance tools is happening for a reason. The global accounting software market is expected to balloon from about $11 billion in 2018 to over $20 billion by 2026. This isn't just a trend; it's a direct solution to the classic problems of manual accounting, where messy workflows and human error always seem to pop up under pressure.

Today's cloud accounting platforms serve as a central hub for all your financial data. They pull everything into one place, creating a single source of truth that your whole team can access, whether they're in the office or working from home.

Automation That Actually Makes a Difference

The real game-changer here is automation. Instead of spending hours manually ticking and tying transactions, software can handle most of the repetitive grunt work. This not only slashes the risk of human error but also frees up your team to do what they do best: analyze the numbers, not just enter them.

Take bank reconciliations, for example. One of the biggest bottlenecks is dealing with PDF bank statements, which often means hours of mind-numbing data entry. This is where specialized tools that convert bank statement PDFs into usable spreadsheets can completely eliminate a tedious task. You save a ton of time and get more accurate data.

My Experience: I once worked with a client who cut their reconciliation time by nearly 75% just by using a simple PDF conversion tool. This one small change allowed their lean team to focus on investigating real discrepancies instead of just keying in numbers.

And that's just one example. To really upgrade your year-end close, you could explore using one of the top document management software for your business to build a central, searchable library for every invoice and receipt. No more digging through file cabinets.

The difference between a manual and an automated close is night and day. It's not just about speed; it's about shifting from reactive data entry to proactive financial management.

Manual vs. Automated Closing Procedures

| Aspect | Manual Closing Process | Automated Closing Process |

|---|---|---|

| Time Investment | High; requires extensive hours for data entry, reconciliation, and cross-checking. | Low; automation handles repetitive tasks, significantly reducing hands-on time. |

| Accuracy | Prone to human error (typos, transposition errors, missed entries). | High; software minimizes errors, ensuring greater data integrity. |

| Real-Time Visibility | Limited; financial picture is only clear after the close is complete. | Excellent; continuous data sync provides up-to-date financial insights at any time. |

| Team Focus | Task-oriented; focused on data entry and procedural tasks. | Strategic; focused on analysis, forecasting, and business advisory. |

| Audit Trail | Difficult to track; relies on physical documents and spreadsheet version control. | Clear and accessible; every transaction and adjustment is digitally logged and auditable. |

Ultimately, adopting technology transforms the finance function. You gain the time and accuracy needed to become a true strategic partner to the business.

Specific Tools for Common Pain Points

Beyond your main accounting software, a whole ecosystem of specialized tools exists to solve those specific headaches that always pop up during the year-end close.

- Expense Tracking Apps: These apps let employees snap a picture of a receipt and submit expenses right away. This puts an end to the last-minute scramble for missing paperwork and helps get expenses coded correctly from the start.

- Automated Accounts Payable (AP) Platforms: These systems can scan invoices, send them for approval, and schedule payments. You can be sure no bill gets lost in the shuffle or paid late.

- Reconciliation Software: Dedicated tools can automatically match thousands of transactions between your books and bank statements, flagging only the exceptions that need a human eye.

Investing in these tools is more than a time-saver; it’s a strategic decision. By automating the mundane tasks, you boost accuracy, get real-time visibility into your finances, and empower your team to provide valuable insights. To dig deeper, check out our guide on accounting automation tools. This shift is what turns a finance team from a group of historical scorekeepers into forward-looking business partners.

Common Questions About the Year End Close

Even the most seasoned finance pros hit a snag or two during the final push to close the books. The pressure is on, and a small uncertainty can feel like a major roadblock. Let's walk through some of the questions I hear most often when it comes to the year end closing procedures.

Having a clear answer ready helps take the mystery out of the process and keeps everything moving forward with confidence. Here’s what business owners and accountants frequently ask.

What Is the Most Common Mistake to Avoid?

Without a doubt, the biggest mistake is procrastination. It's so tempting to treat the year-end close as a "future me" problem, putting off gathering documents and reconciling accounts until the last possible minute. That eleventh-hour rush is a recipe for stress, burnout, and costly errors.

A smooth close isn't a one-time event; it’s the payoff for consistent, disciplined bookkeeping all year long. The formal closing process should really kick off at least a month or two before your fiscal year ends, not after it's already over.

The best defense against a chaotic year-end is a proactive offense. Start early, map out a detailed timeline with clear owners for each task, and actually stick to it. This simple discipline turns the close from a frantic scramble into a predictable, manageable project.

Starting early gives you the breathing room to find and fix discrepancies without the panic of a looming deadline.

How Long Should This Process Take?

There's no magic number here. The timeline for a year-end close can swing wildly depending on a few key things:

- Company Size: A small shop with a few hundred transactions will close the books much faster than a large corporation with multiple divisions.

- Transaction Volume: More transactions simply mean more work to reconcile and review. It's a direct correlation.

- Level of Automation: This is the game-changer. Companies using modern accounting software and automation tools can close their books in a fraction of the time.

For a small, well-organized business, the process might only take one to two weeks. For a larger, more complex company still relying on manual processes, it can easily stretch to four weeks or even longer. Investing in technology to automate tasks like reconciliations can often cut that closing period in half.

Understanding a Soft Close vs. a Hard Close

You'll often hear accountants talk about a "soft close" and a "hard close," and the distinction is important. Think of them as two different levels of finality in your accounting cycle.

A soft close is what you do at the end of each month or quarter. The goal is to reconcile major accounts (like cash) and get internal financial reports ready for management. During a soft close, some accruals and adjustments might be estimated just to get a quick snapshot of performance. It’s about speed and timely insight, not audit-level perfection.

A hard close, on the other hand, is the official, formal year-end close. This process is much more rigorous. It requires every single account to be fully reconciled, all necessary adjusting entries to be posted, and the final, audit-ready financial statements to be locked down. Once the hard close is done, the books for that year are officially closed for business—no more changes.

Stop wasting hours on manual data entry from PDF bank statements. Bank Statement Convert PDF transforms locked documents into clean, usable Excel files in seconds, slashing your reconciliation time and eliminating errors. See how much time you can save by visiting us at https://bankstatementconvertpdf.com.